Where Multi Cap Funds Fit in a Wealth Plan

Multi Cap funds are mandated by SEBI to maintain a minimum 25% allocation each across large, mid, and small cap companies at all times. Unlike Flexi Cap funds, where the manager has full discretion over cap-size allocation, Multi Cap funds carry a structural obligation to diversify across all three market segments — regardless of market conditions.

This mandatory diversification is both the category’s strength and its constraint.

Within the RSW Financial Independence Framework, Multi Cap funds serve a specific role:

- Accumulate Wealth: Growth engine for CORE life goals — retirement, children’s education, and long-term corpus — where broad market participation across cap sizes drives compounding over 7–10 year horizons.

- Accelerate Wealth: Satellite allocation for investors seeking alpha beyond a Flexi Cap or Large Cap core, with structured exposure to mid and small cap segments without the concentration risk of a pure mid or small cap fund.

Multi Cap funds are not interchangeable with Flexi Cap funds. The mandatory 25-25-25 structure means the investor always carries mid and small cap exposure — a feature that increases return potential and volatility simultaneously. This is appropriate for investors who understand and accept that trade-off within a structured plan.

The 5-Parameter Evaluation Framework

Fund selection follows five structured parameters. A fund must satisfy all five to qualify as a core holding.

| Parameter | What It Measures | Why It Matters in Wealth Planning |

|---|---|---|

| Risk-Adjusted Returns | Sharpe & Sortino Ratios | Efficiency of return generation, not just quantum |

| Consistency | Rolling 3Y/5Y/7Y returns across cycles | Prevents performance-chasing; ensures structural capability |

| Volatility & Downside Risk | Std Dev, Beta & Max Drawdown | Protects compounding continuity during corrections |

| Cost Structure | Expense ratio & exit load | Cumulative drag on long-horizon SIP compounding |

| Fund Stability | AUM, fund age, manager tenure | Confirms cycle-tested credibility and strategy continuity |

Top 5 Multi Cap Funds — 2026 Evaluation

| Fund | Mean Return (%) | Sharpe | Sortino | Alpha | Beta | Std Dev (%) | Expense Ratio (%) | Portfolio Turnover (%) |

|---|---|---|---|---|---|---|---|---|

| Axis Multicap | 20.78 | 0.92 | 1.13 | 4.16 | 0.91 | 16.04 | 2.29 | 50.00 |

| Nippon India Multi Cap | 19.94 | 0.87 | 1.20 | 3.45 | 0.90 | 16.00 | 1.62 | 28.00 |

| Kotak Multicap | 22.34 | 0.92 | 1.11 | 4.43 | 1.02 | 17.86 | 1.64 | 44.41 |

| ICICI Pru Multicap | 19.93 | 0.87 | 1.24 | 3.33 | 0.91 | 16.08 | 1.67 | 94.00 |

Risk ratios and fund data as of May 2026. Past performance does not guarantee future results. Source: Value Research.

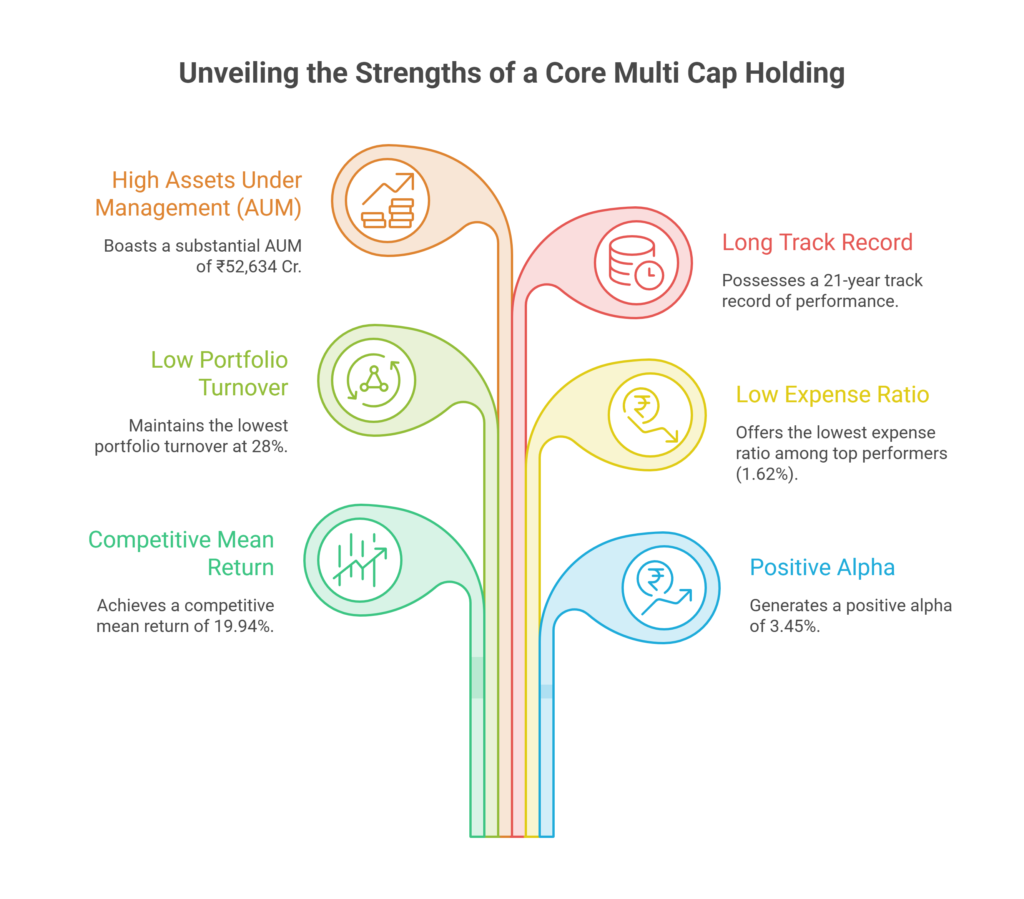

Nippon India Multi Cap — Core Portfolio Anchor

The strongest overall case for a core Multi Cap holding. Competitive mean return (19.94%), positive alpha (3.45%), and the lowest portfolio turnover in the group (28%) — signalling a disciplined, low-churn strategy that supports tax efficiency. The lowest expense ratio among the top performers at 1.62%, combined with an AUM of ₹52,634 Cr and a 21-year track record, makes this the most cycle-tested fund in the category.

Wealth management role: Primary Multi Cap allocation within the Accumulate Wealth stage. Best combination of cost efficiency, stability, and cycle-validated performance.

Kotak Multicap — Highest Returns, Beta Above 1

Leads the group on mean return (22.34%) and alpha (4.43%), tied for the highest Sharpe (0.92). However, a beta of 1.02 is the only fund in this evaluation that moves more than the broader market — amplifying both upside and downside. The portfolio turnover (44.41%) and a short track record of 4Y 7M limit the depth of cycle validation.

Wealth management role: High-conviction secondary allocation for growth-oriented investors within the Accelerate Wealth stage. Not recommended as a standalone core holding given the limited track record and above-market beta.

Axis Multicap — Strong Risk-Adjusted Profile, High Cost

Matches Kotak on Sharpe (0.92) and delivers strong alpha (4.16) with a below-market beta (0.91). However, the expense ratio at 2.29% is among the highest in the group and the fund is only 4Y 4M old — with no cycle downturn on record. The cost-return trade-off requires explicit justification.

Wealth management role: Tactical secondary allocation where Nippon India is the core. Warrants review if the expense ratio does not normalise as AUM grows.

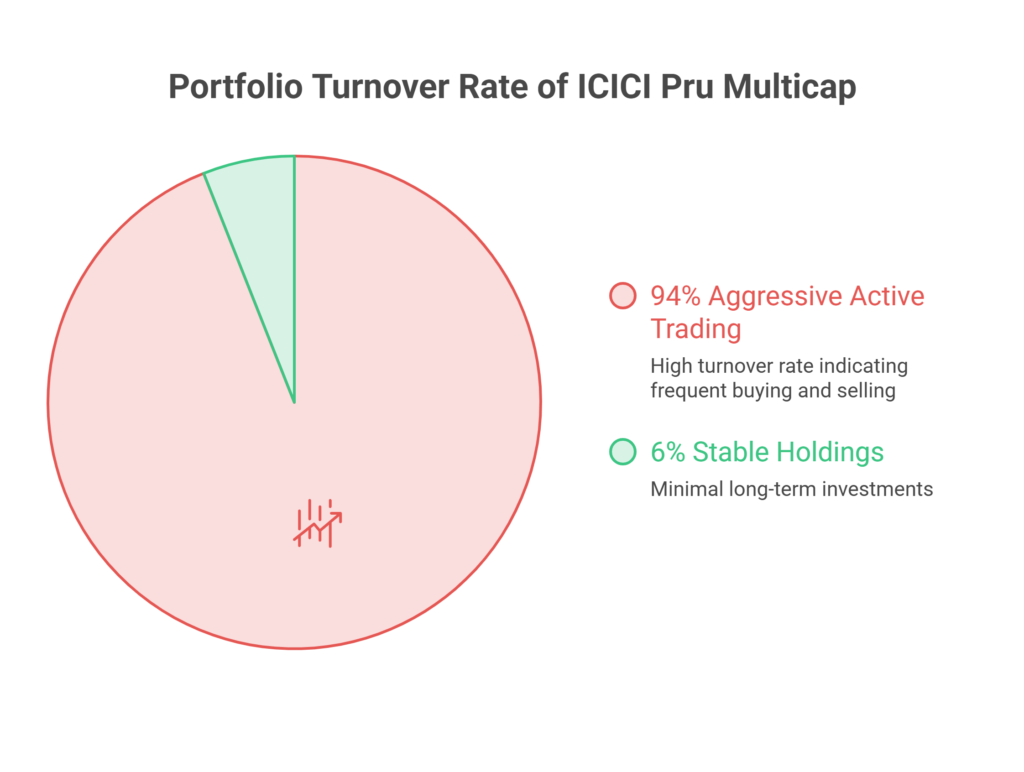

ICICI Pru Multicap — Longest Track Record, High Churn

The only fund in this evaluation with a 31-year history — providing the deepest cycle validation by a significant margin. Risk metrics are sound: Sharpe of 0.87, Sortino of 1.24, and a controlled beta of 0.91. The concern is structural: a portfolio turnover of 94% signals aggressive active trading, which increases transaction costs and potential tax drag beyond what the expense ratio alone reflects.

Wealth management role: Suitable as a secondary allocation for investors who prioritise institutional track record. The turnover rate should be factored into the true cost of ownership before inclusion.

A Critical Observation: Track Record and the New Fund Risk

Three of the four funds evaluated — Axis Multicap (4Y 4M), Kotak Multicap (4Y 7M), — have limited or unverified cycle history. The Multi Cap category itself was restructured by SEBI in 2020, meaning most funds in this space have never operated through a full bull-bear cycle under the current mandate.

This creates a material selection risk:

| Fund Age Profile | Risk Implication | Recommended Action |

| Under 5 years | No bear cycle validation under current mandate | Treat as satellite only; not core |

| 5–15 years | Partial cycle data | Use as secondary with active monitoring |

| 15+ years | Meaningful cycle history | Eligible for core allocation |

Only Nippon India Multi Cap (21Y) and ICICI Pru Multicap (31Y) meet the threshold for core consideration on track record alone.

Positioning Multi Cap Funds by Goal

| Goal | Recommended Funds | Complementary Instruments |

|---|---|---|

| Long-Term Wealth Corpus — 10Y+ | Nippon India Multi Cap | Flexi Cap as primary equity core |

| Accumulate Wealth — CORE goal funding | Nippon India + ICICI Pru Multicap | NPS for retirement layer |

| Accelerate Wealth — alpha beyond core | Kotak Multicap as satellite | Flexi Cap or PMS as primary |

FAQ’s

A: Check the actual allocation first. If your Flexi Cap fund is holding 70%+ in Large Caps, it is behaving more like a Large Cap fund — in which case a Multi Cap fund adds the structural mid and small cap exposure you are missing.

If your Flexi Cap fund already holds 30%+ across mid and small caps, adding a Multi Cap fund creates overlap without meaningful diversification benefit.

A: Either can serve as core — but for different reasons. Flexi Cap gives you manager discretion; Multi Cap gives you structural diversification through the mandatory 25-25-25 allocation.

For investors who want guaranteed mid and small cap participation without relying on a fund manager’s allocation decision, Multi Cap is the stronger core choice. For investors who trust active management to allocate dynamically, Flexi Cap is preferable.

A: For investors in the Accumulate Wealth stage, Multi Cap can form 30–50% of total equity allocation — either as a standalone core or alongside a Flexi Cap fund. The mandatory mid and small cap exposure means it carries higher volatility than a Large Cap or Flexi Cap core, so the allocation must be sized to your risk capacity and goal horizon. Never combine Multi Cap with a dedicated Mid Cap and Small Cap fund without checking for overlap.

A: Taxation is identical — LTCG at 12.5% for gains held over 12 months with ₹1.25 lakh annual exemption, and STCG at 20% under 12 months. Yes — switching from a Flexi Cap fund to a Multi Cap fund is a redemption event and triggers capital gains tax immediately.

Given that the Multi Cap category was restructured in 2020, many investors are switching from older Flexi Cap holdings — always calculate the tax cost before making the move.

A: Begin systematic transfers 3–4 years before a goal deadline — slightly earlier than Flexi Cap due to the structural mid and small cap exposure. The mandatory 25% small cap allocation means Multi Cap funds can drawdown 35–45% during corrections and take longer to recover than a pure Flexi Cap fund. A phased shift into hybrid or debt funds starting 3–4 years out protects your corpus from sequence-of-returns risk at the goal finish line.

In the Multi Cap category, the mandatory 25-25-25 structure means the investor permanently carries mid and small cap risk — irrespective of market conditions. This is not a default choice for conservative or goal-proximate investors.

The right Multi Cap allocation depends on where you are in the RSW framework, what role this fund plays relative to your existing equity exposure, and whether your goal horizon can absorb the higher volatility that comes with structural mid and small cap participation.

Fund quality is one input. Your Wealth Personality, your current stage in the RSW Framework, and your specific goal timelines determine the right combination.

Book your free wealth planning consultation →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years