Where Small Cap Funds Fit in a Wealth Plan

Small Cap funds invest in companies ranked 251st and beyond by market capitalisation — businesses in early to mid stages of their growth journey, with significant upside potential and equally significant execution risk. This segment offers the highest return premium across all equity categories, but demands the longest horizon, the highest volatility tolerance, and the most disciplined investor behaviour in return.

Within the RSW Financial Independence Framework, Small Cap funds occupy a very specific and non-negotiable position:

- Accumulate Wealth: A small, disciplined satellite allocation — never the core — for investors with a 10+ year horizon whose CORE goal funding is already structured through Flexi Cap and Mid Cap holdings.

- Accelerate Wealth: Alpha generation layer for investors expanding beyond CORE investments, where a higher-risk, higher-reward allocation is appropriate and affordable within the overall portfolio architecture.

Small Cap funds do not belong in every portfolio. They belong only after the Build Safety Net stage is fully complete — emergency fund, term insurance, and health insurance in place — and only for investors whose goal timelines can absorb a 50–60% drawdown without triggering a panic exit or goal disruption.

The 5-Parameter Evaluation Framework

Fund selection follows five structured parameters. A fund must satisfy all five to qualify as a core holding.

| Parameter | What It Measures | Why It Matters in Wealth Planning |

|---|---|---|

| Risk-Adjusted Returns | Sharpe & Sortino Ratios | Efficiency of return generation, not just quantum |

| Consistency | Rolling 3Y/5Y/7Y returns across cycles | Prevents performance-chasing; ensures structural capability |

| Volatility & Downside Risk | Std Dev, Beta & Max Drawdown | Protects compounding continuity during corrections |

| Cost Structure | Expense ratio & exit load | Cumulative drag on long-horizon SIP compounding |

| Fund Stability | AUM, fund age, manager tenure | Confirms cycle-tested credibility and strategy continuity |

Top 5 Small Cap Funds — 2026 Evaluation

| Fund | Mean Return (%) | Sharpe | Sortino | Alpha | Beta | Std Dev (%) | Expense Ratio (%) | Fund Age | Portfolio Turnover (%) |

|---|---|---|---|---|---|---|---|---|---|

| Bandhan Small Cap | 29.02 | 1.10 | 1.77 | 9.29 | 0.92 | 20.93 | 2.00 | 6Y 2M | 22.00 |

| Invesco India Smallcap | 23.75 | 0.91 | 1.13 | 5.23 | 0.84 | 19.62 | 1.93 | 7Y 6M | 46.00 |

| HDFC Small Cap | 16.94 | 0.60 | 0.87 | -0.87 | 0.79 | 18.26 | 1.64 | 18Y 1M | 7.59 |

| Nippon India Small Cap | 21.24 | 0.77 | 1.15 | 2.22 | 0.87 | 19.77 | 1.35 | 15Y 8M | 17.00 |

| Quant Small Cap | 20.53 | 0.71 | 1.21 | 1.34 | 0.88 | 20.49 | 2.02 | 29Y 5M | 151.00 |

Risk ratios and fund data as of May 2026. Past performance does not guarantee future results. Source: Value Research.

Nippon India Small Cap — Core Portfolio Anchor

The strongest overall case for a core Small Cap holding. The largest AUM in the category at ₹72,673 Cr combined with a 15-year track record provides the deepest cycle validation among newer peers. Expense ratio of 1.35% is the lowest in the group — a meaningful compounding advantage over a 10+ year horizon. Portfolio turnover of 17% signals a disciplined, low-churn strategy. While the Sharpe (0.77) and alpha (2.22) are moderate, the combination of scale, cost efficiency, and track record makes it the most structurally sound choice for a core allocation.

Wealth management role: Primary Small Cap allocation within the Accumulate Wealth stage for investors with a 10+ year horizon. Best cost-efficiency and stability profile in the category.

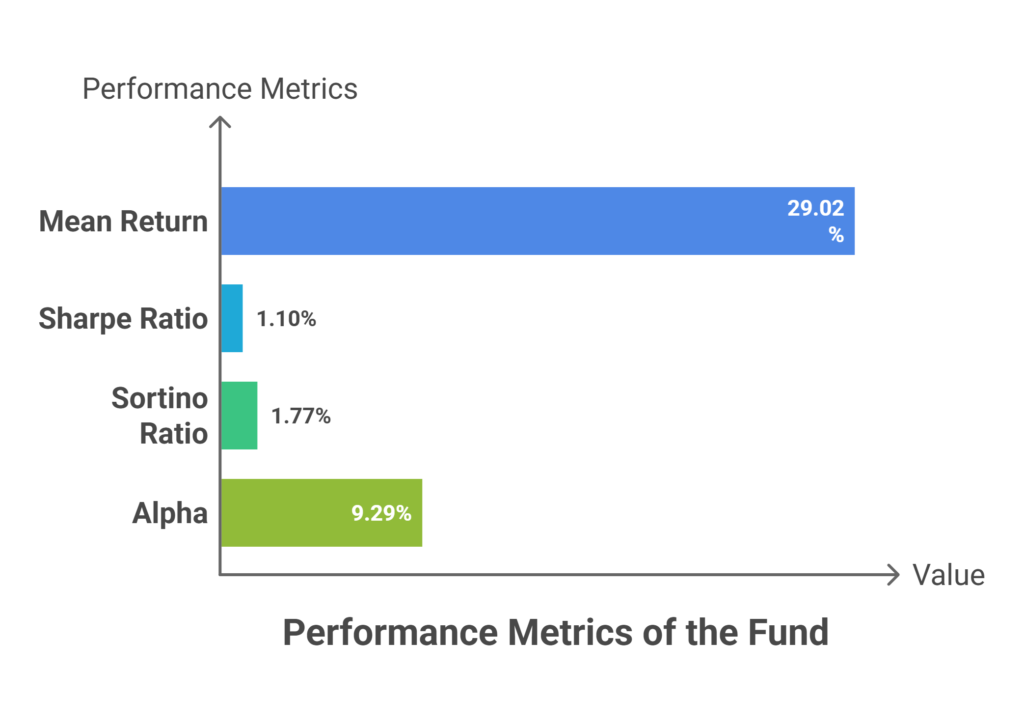

Bandhan Small Cap — Highest Alpha, Shortest Track Record

Leads the group comprehensively on return metrics: highest mean return (29.02%), Sharpe (1.10), Sortino (1.77), and alpha (9.29) by a significant margin. However, a fund age of just 6Y 2M is the critical constraint — this fund has never operated through a full bear market cycle. The exceptional returns have been generated in a predominantly bull market environment, which limits the reliability of the track record for long-term wealth planning purposes.

Wealth management role: High-conviction satellite allocation within the Accelerate Wealth stage only — and only for investors who understand the track record limitation. Not suitable as a primary Small Cap holding until the fund demonstrates cycle resilience through a sustained correction.

Invesco India Smallcap — Promising Profile, High Churn

Strong alpha (5.23) and below-market beta (0.84) suggest genuine stock-picking capability with partial downside protection. However, portfolio turnover of 46% is the second highest in the group — raising questions about transaction cost drag and tax efficiency over a long horizon. At 7Y 6M, the track record remains limited for a category that demands cycle validation.

Wealth management role: Tactical secondary allocation within the Accelerate Wealth stage. Monitor whether alpha persists net of the elevated churn cost before committing as a structural holding.

HDFC Small Cap — Track Record Without Alpha

The second-longest track record in the group at 18Y 1M and the lowest portfolio turnover (7.59%) — both strong structural attributes. However, a negative alpha of -0.87 is a definitive concern. The fund is underperforming its benchmark on a risk-adjusted basis despite active management. In the Small Cap category, where the return premium over Large Cap is the primary justification for higher risk, a fund that cannot generate positive alpha does not earn its place in a structured wealth plan.

Wealth management role: Not recommended as an active holding. Investors in this fund should evaluate a Nifty Smallcap 250 Index Fund as a lower-cost alternative — particularly given the fund’s near-zero alpha does not justify active management fees.

Quant Small Cap — Highest Turnover, Highest Risk

The longest track record in the group at 29Y 5M provides meaningful cycle validation — a genuine differentiator. However, a portfolio turnover of 151% is the most extreme figure across all five equity categories evaluated in this series. At this churn rate, the fund is effectively replacing its entire portfolio more than once a year — generating transaction costs and capital gains events that significantly erode the net return to the investor. The highest expense ratio (2.02%) compounds this further.

Wealth management role: The track record is the fund’s only compelling argument. The cost structure — active management fees plus turnover-driven transaction drag — makes it difficult to justify over a lower-cost, lower-churn alternative. Approach with caution and only after a full cost-adjusted return analysis.

A Critical Observation: Track Record and the Small Cap Trap

Three of the five funds evaluated — Bandhan (6Y 2M), Invesco (7Y 6M), and to a lesser extent Nippon India (15Y 8M) — have generated their strongest returns in a period dominated by small cap outperformance. The real test of a Small Cap fund is how it behaves during a sustained small cap bear market — a period that can last 3–5 years and produce drawdowns of 50–60%.

| Fund Age Profile | Risk Implication | Recommended Action |

|---|---|---|

| Under 8 years | Bull market returns only — no bear cycle validation | Satellite only; never core |

| 8–15 years | Partial cycle data | Secondary with active monitoring |

| 15+ years | Meaningful cycle history | Eligible for core consideration |

Only Nippon India (15Y 8M), HDFC Small Cap (18Y 1M), and Quant Small Cap (29Y 5M) cross the minimum threshold — and of these, only Nippon India passes both the track record and alpha test.

Positioning Small Cap Funds by Goal

| Goal | Recommended Funds | Complementary Instruments |

|---|---|---|

| Long-Term Wealth Corpus — 12Y+ | Nippon India Small Cap | Flexi Cap as primary core + Mid Cap as growth layer |

| Accumulate Wealth — satellite allocation | Nippon India Small Cap | Never more than 15–20% of total equity allocation |

| Accelerate Wealth — alpha generation | Bandhan Small Cap as high-conviction satellite | Flexi Cap + Mid Cap as primary equity core |

A Fund Selection Is Not a Wealth Plan

Small Cap funds carry the highest risk across all equity categories evaluated in this series. They are appropriate for a minority of investors — those who are well into the Accumulate Wealth stage, have their CORE goals fully funded, and have a genuine 12+ year horizon with the behavioural discipline to hold through a 50% drawdown without exiting.

For most investors building wealth through SIPs, a Flexi Cap and Mid Cap combination delivers the majority of the equity return premium without the concentration risk of Small Cap exposure.

Fund quality is one input. Your Wealth Personality, your current stage in the RSW Framework, and your specific goal timelines determine whether Small Cap belongs in your portfolio at all — and if so, in what proportion.

Q: If my Flexi Cap fund already holds Small Cap stocks, do I need a separate Small Cap fund?

A: Check the actual allocation first. Most Flexi Cap funds hold less than 10% in Small Caps — in which case a dedicated Small Cap fund adds meaningful exposure. However, given the liquidity risk and depth of drawdowns in this category, a separate Small Cap fund is only appropriate after your Flexi Cap and Mid Cap core is already in place. Small Cap is the last layer — not the first.

Q: Should Small Cap be part of my core holding or strictly a satellite?

A: Strictly a satellite — never the core. Small Cap funds experience drawdowns of 50–60% during corrections and may take years to recover from market downturns. Placing Small Cap as your core equity holding exposes your entire wealth plan to this recovery risk. Flexi Cap is the core; Mid Cap is the growth layer; Small Cap is the high-conviction satellite — in that order.

Q: How much of my equity portfolio should be allocated to a Small Cap fund?

A: Not more than 15–20% of total equity allocation — and only for investors firmly in the Accumulate Wealth or Accelerate Wealth stage with a 12+ year horizon. Given the highly volatile nature of Small Cap funds, investments should not be concentrated in Small Cap alone — the allocation must sit within a portfolio that already has Flexi Cap and Mid Cap as stabilising anchors.

Q: At what stage of my wealth plan should I exit a Small Cap fund?

A: Earlier than any other equity category — begin systematic transfers at least 5 years before a goal deadline, not 3. Small Cap funds can drawdown 50–60% and take 3–5 years to fully recover. Waiting until 3 years out — as you might with Flexi Cap — leaves your corpus dangerously exposed to a correction at exactly the wrong time. A phased shift into Mid Cap first, then hybrid, then debt, over a 5-year exit runway is the structurally correct approach.

Book your free one-hour wealth planning call →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”