If you are a salaried professional between 30 and 50, wealth creation is no longer optional — it is strategic.

Generate Income.

Allocate Capital

Think Ahead

But without a structured wealth planning framework, investments remain disconnected from life goals.

The RSW Financial Independence Framework is a structured financial planning framework designed specifically for salaried professionals who want:

- Financial stability

- Goal-based investing

- Retirement readiness

- Long-term wealth creation

- Generational continuity

This is not about chasing returns. It is about building a system.

1. Why Salaried Professionals Need a Structured Wealth Planning Framework

Salaried income is predictable — but finite.

You have:

- Fixed earning years

- Rising lifestyle costs

- Education inflation

- Retirement dependency on accumulated assets

Unlike business owners, your wealth depends on disciplined allocation of surplus income.

A structured wealth planning framework ensures:

- Every investment funds a goal

- Risk is controlled before growth

- Retirement corpus is calculated — not assumed

- Capital grows with direction

Without structure, wealth planning becomes fragmented.

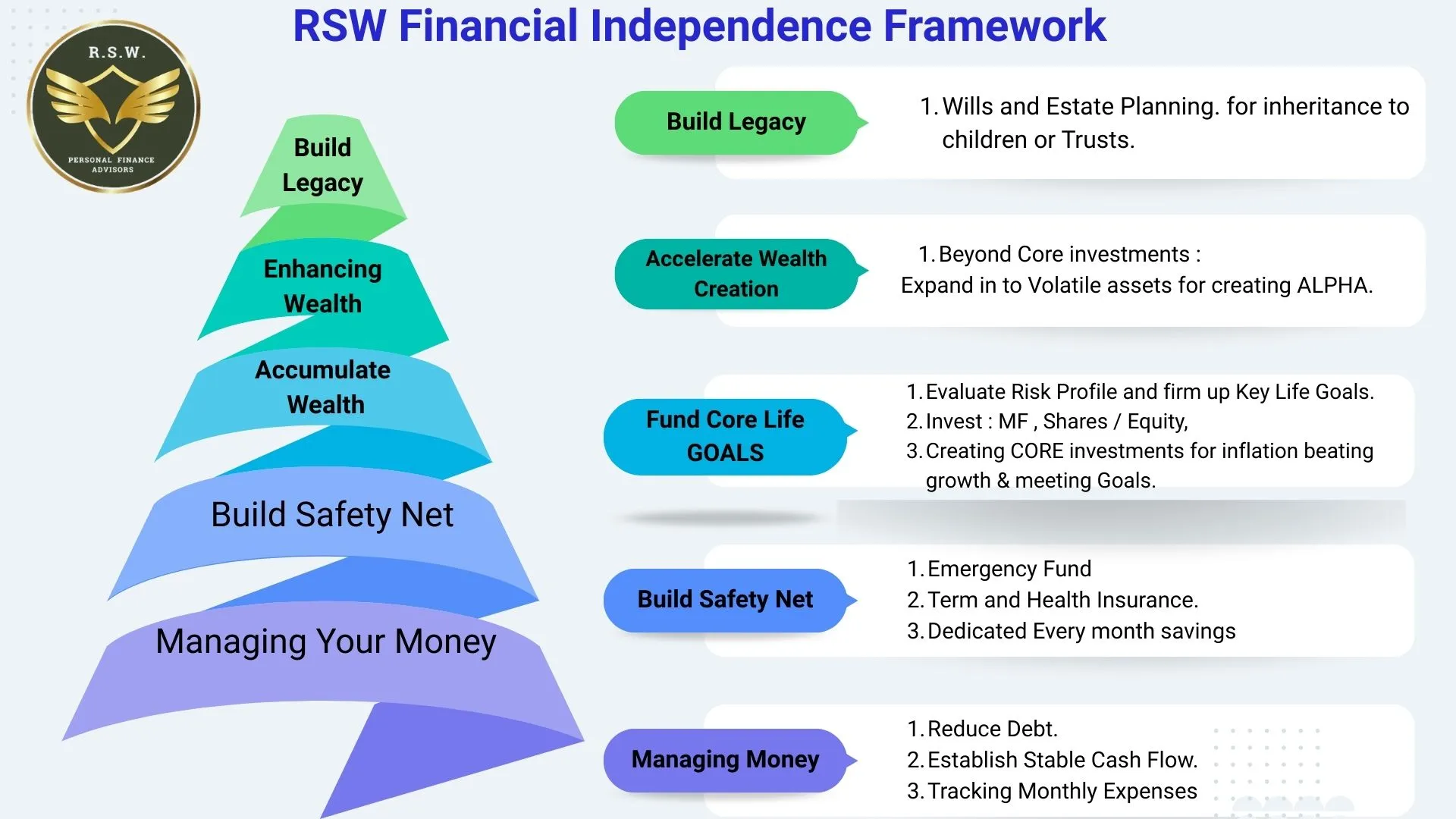

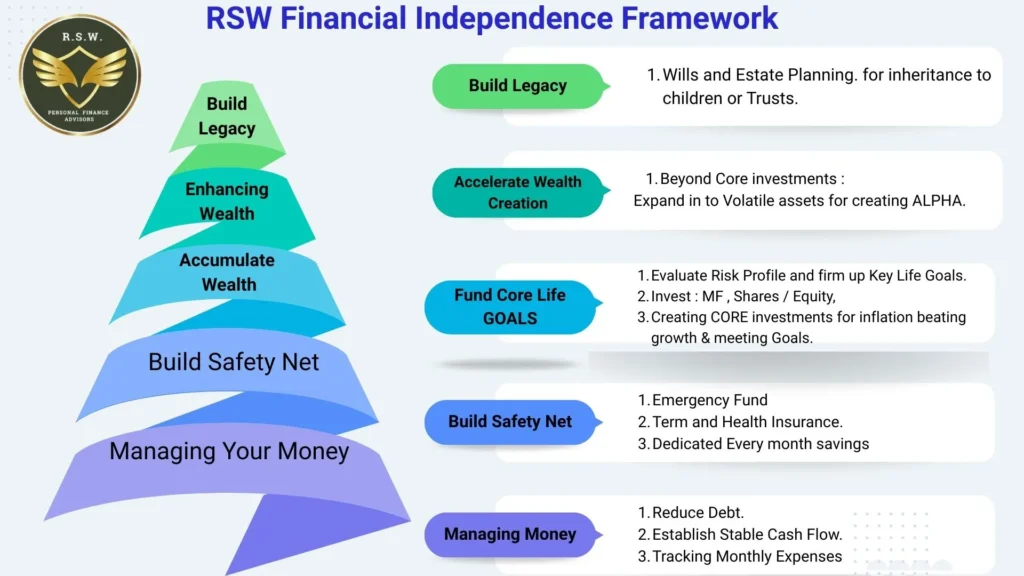

2. The 5-Stage Wealth Planning Framework for Financial Independence

The RSW Financial Independence Framework operates in sequence. Each stage strengthens the next.

Stage 1: Cash Flow & Money Management for Salaried Professionals

Before investing, control must exist.

This stage focuses on:

- Expense optimization

- Debt rationalization

- Surplus creation

- Automated savings discipline

Wealth planning begins with surplus power.

If monthly surplus is unstable, long-term investing collapses during stress. This is the foundation of personal financial planning.

Stage 2: Emergency Fund & Risk Protection Strategy

No wealth planning framework is complete without risk control.

This stage includes:

Maintain 6–8 months of expenses in liquid instruments.

This protects:

- EMIs

- Education savings

- Retirement investments

Insurance Planning

- Term insurance aligned to income and liabilities

- Health insurance independent of employer cover

Risk protection ensures that financial planning survives life events.

Without this stage, compounding remains fragile.

Stage 3: Goal-Based Financial Planning

3. Fund Core Life Goals — Home, Children’s Education & Retirement

This is the structural core of the wealth planning framework.

For salaried professionals, three goals dominate long-term planning.

Each goal has a different time horizon, risk profile, and instrument fit — which is why understanding your Wealth Personality matters before you allocate a single rupee.

3a. Home Ownership Planning

A primary residence provides stability, lifestyle continuity, and a tangible asset. But in wealth planning, how you fund it matters as much as owning it.

Sustainable wealth planning around home ownership requires:

- An EMI that does not exceed 35–40% of your take-home income

- Preserved liquidity — your emergency fund must survive the down payment

- A balanced asset allocation so your entire net worth is not locked in one illiquid asset

For the accumulation phase — building your down payment corpus — debt mutual funds and hybrid funds offer stability with better post-tax returns than FDs for a 3–5 year horizon.

[Read our Mutual fund planning guide →]

Real estate should support your financial independence — not distort it.

3b. Children’s Education Planning

Education costs in India are rising at 10–12% annually — well above general inflation. A plan built without numbers is not a plan.

Effective education planning requires:

- Inflation-adjusted corpus projections (not a round number guess)

- Time-bound allocation matched to when the goal falls due

- Progressive de-risking as the goal approaches — shifting from equity to debt in the final 2–3 years

How each instrument fits this goal:

Mutual Funds are the primary vehicle — a dedicated SIP in an equity fund started early gives compounding the time it needs. For a 10+ year horizon, flexi cap or multi cap funds work well.

For a 5–7 year horizon, hybrid funds reduce volatility risk. [Goal-based Equity mutual fund planning →]

ETFs — specifically Nifty 50 or index ETFs — work well as a low-cost passive layer in a longer education corpus, reducing expense drag over a decade-long horizon. [ETF investing in India →]

Smallcases can supplement the core MF allocation for investors with a growth-oriented Wealth Personality — adding thematic or factor-based equity exposure alongside the core SIP.

SIPs without calculation are not planning. Goal-linked allocation is.

3c. Retirement Planning for Salaried Professionals

Retirement is the only financial goal you cannot delay indefinitely, cannot borrow for, and cannot outsource to anyone else. It demands the most disciplined, long-horizon approach in your entire wealth plan.

A proper retirement strategy is built on:

- A lifestyle-based corpus calculation — not a generic “₹1 crore is enough” assumption

- Inflation modelling at 6–7% annually over a 25–30 year post-retirement period

- Asset allocation discipline that maintains long-term equity exposure without panic-driven exits

- A withdrawal strategy (SWP) that converts your corpus into a predictable income stream

3d. How each instrument fits this goal:

Mutual Funds form the backbone —

Flexi Cap funds for long-term equity growth,

Hybrid funds for volatility control in the decade approaching retirement, and

Debt funds for capital preservation post-retirement.

NPS (National Pension System) offers tax efficiency under Section 80CCD and a disciplined, lock-in structure that prevents premature withdrawal — making it an excellent complement to your MF retirement corpus.

[Designing your NPS strategy →]

ETFs serve as a low-cost passive equity layer — index ETFs reduce cost drag on the portion of your corpus that simply needs to track market returns over 20+ years. [ETF investing in India →]

PMS (Portfolio Management Services) becomes relevant for investors with a larger accumulated corpus — typically ₹50L+ — who want a more actively managed, research-driven equity strategy to accelerate wealth creation in their peak earning years. [Portfolio Management Services →]

SIFs (Specialised Investment Funds) are worth understanding for investors approaching a ₹10L+ annual investable surplus — a newer SEBI category offering strategy depth beyond standard MF categories.

Your Wealth Personality shapes how you combine these — whether you lean toward a passive, low-cost ETF-heavy structure, an actively managed MF core, or a blended approach.

Retirement planning is not just a financial goal. It is the truest definition of financial independence.

Beyond all these, for those conservative investors, who are comfortable with their FD’s, there is an alternate option of investing in Co-Operative Societies. They offer higher interest rates. Read about them.

Stage 4: Wealth Creation & Capital Growth Strategy

Once core goals are structured, expansion begins.

This stage enhances returns without destabilizing financial planning.

It includes:

- Blue-chip stock ownership

- Core and Tactical asset allocation

- Portfolio rebalancing

- Tax efficiency optimization

This is where structured wealth creation accelerates. Most investors attempt this stage prematurely.

In a proper wealth planning framework, growth follows structure.

Stage 5: Estate Planning & Legacy Strategy

Financial independence extends beyond retirement.

True wealth planning includes:

- Will structuring

- Trust planning

- Succession design

- Tax-efficient inheritance

Estate planning converts personal wealth into generational continuity.

Without legacy structuring, wealth lacks permanence.

3. How This Wealth Planning Framework Creates Financial Independence

The RSW Financial Independence Framework ensures:

- Protection precedes growth

- Goals precede allocation

- Structure precedes performance

- Sequence precedes scale

Each stage builds resilience.

Resilience builds wealth.

Wealth builds independence.

Financial independence is not a feeling of comfort. It is a funded structure where:

- Home is secure

- Education is planned

- Retirement corpus is visible [Designing NPS Strategy]

- Risks are covered

- Investments are aligned

4. Who This Financial Planning Framework Is Designed For ?

This system is built specifically for:

- Salaried professionals aged 30–50

- Dual-income households

- Families planning children’s education

- Individuals serious about retirement planning

- Investors seeking structured wealth creation

It is not for speculative traders. It is for disciplined wealth builders

5. Implementing the RSW Financial Independence framework

If you are already investing, the key question is not performance.

The question is structure.

Are your investments aligned to:

- Retirement planning?

- Children’s education planning?

- Home ownership planning?

- Long-term wealth creation?

Or are they simply performing in isolation?

A structured review through the lens of the Wealth Planning Framework for Salaried Professionals can clarify this.

Financial independence is engineered — not improvised.

You now know the framework. The next step is finding out where you stand within it.

Most salaried professionals are somewhere between Stage 2 and Stage 4 — with gaps they are not aware of. An unreviewed insurance cover. A goal without a corpus. A portfolio growing without a plan behind it.

A one-hour call is enough to map your current position, identify the gaps, and give you a clear sequence of what to do next.

No commitment. No products pushed. Just clarity.

Book your free one-hour wealth planning call →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”