Most Indian salaried investors do not fail because they picked the wrong mutual fund. They fail because they could not stay with the plan when markets moved.

When the Nifty fell 15% in a matter of weeks, they moved their equity SIPs to liquid funds. When a sector fund delivered 40% in a year, they shifted their entire surplus into it.

When interest rates rose, they exited their debt funds without understanding why they held them in the first place.

These are not investment failures. They are behaviour failures.

And Core and Tactical allocation, understood correctly, is the structural answer to this problem.

The Real Problem Is Not Knowledge — It Is Architecture

Most salaried investors between 30 and 50 know what they should do.

They know equities outperform over the long term. They know SIPs should not be stopped during corrections. They know chasing last year’s top performer is a bad idea.

Yet they do it anyway. Why?

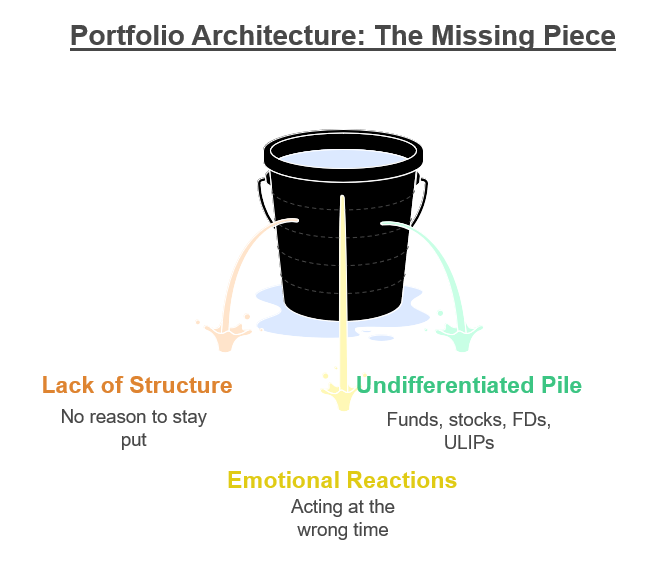

Because their portfolio has no architecture.

Everything sits in one undifferentiated pile — some mutual funds here, a few stocks there, an FD from three years ago, a ULIP someone sold them.

When markets move, there is no structural reason to stay put. So they act.

And acting at the wrong time is what destroys long-term wealth.

Core and Tactical allocation gives your portfolio a spine.

It creates two distinct buckets with two distinct purposes — and more importantly, two distinct sets of rules for when you are and are not allowed to touch them.

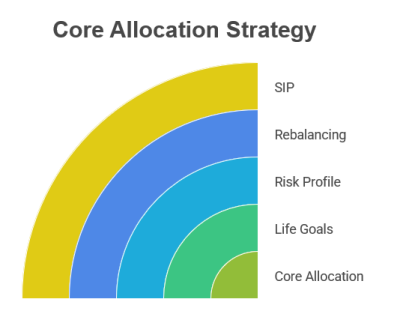

Core Allocation: Your Behavioural Anchor

Core is not simply your long-term bucket. It is your behavioural anchor.

The purpose of Core allocation is to hold the investments that are tied directly to your life goals — retirement, children’s education, financial independence — and to protect them from your own short-term reactions to market noise.

Core allocation typically spans a 7 to 10-year horizon or longer. It is built around your risk profile and rebalanced periodically — not because you have a market view, but to restore the original structure.

The rule is simple: you do not touch your Core based on what the market is doing.

This single rule — if followed — eliminates the most destructive investor behaviour: selling good assets at the wrong time.

For a salaried professional with a ₹30,000 monthly surplus and two EMIs, the Core is where the majority of that surplus flows, consistently, month after month, through an SIP structure that removes the decision entirely.

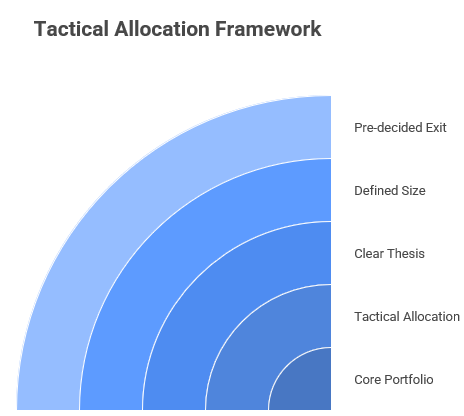

Tactical Allocation: Your Pressure Valve

Here is something rarely acknowledged: most investors tamper with their Core not because they are greedy, but because they feel they have no other outlet.

When gold rallied 30% in 2024, the investor with no tactical framework had two choices — jump in and disturb the Core, or do nothing and feel like they missed out. Both options are unsatisfying.

Tactical allocation solves this by creating a legitimate, bounded space for opportunistic moves. It is the pressure valve that protects the Core.

Tactical allocation operates on a 6 to 12-month horizon with three non-negotiable rules:

- A clear thesis. Why are you making this move? What specific market condition or valuation signal is driving it?

- A defined size. Tactical positions should represent 20 to 30% of your portfolio at most. They should never be large enough that a wrong call damages your Core.

- A pre-decided exit. Before you enter a tactical position, you decide when you will exit — either when the thesis plays out or when it clearly has not.

Without these three rules, Tactical allocation is just another name for speculation.

Where Does Your Investment Belong? A Practical Classification

This is the question every reader will have after understanding the framework: where do my existing investments actually fit?

The table below classifies the most common Indian investment options. Each is linked to a dedicated article for deeper reading.

Use this as a reference to audit your own portfolio.

| Investment Option | Classification | Why |

|---|---|---|

| Nifty 50 / Sensex Index Fund | Core | Broad market, low cost, long-term compounder |

| Large-cap Mutual Fund | Core | Stable, diversified, goal-aligned |

| PPF / EPF | Core | Tax-efficient, long-duration, non-negotiable |

| Term Insurance | Core | Protection layer, not an investment |

| Balanced Advantage Fund | Core | Built-in rebalancing, suits passive investors |

| Debt Mutual Fund — Long Duration | Core | Stability and income over 3+ year horizon |

| Real Estate — Self-occupied | Core | Long-duration asset, goal-linked |

| Mid-cap / Small-cap Fund | Core + Tactical* | Core if held via SIP for 7+ years; Tactical if lump sum on correction |

| Sector / Thematic Fund | Tactical | Time-bound thesis, high concentration risk |

| Gold ETF | Tactical | Short-term positioning on macro or geopolitical thesis |

| International Fund | Tactical | Currency and diversification play, time-bound |

| Short Duration Debt Fund | Tactical | Interest rate cycle positioning |

| Real Estate — Rental / Commercial | Tactical | Opportunistic entry, income-generating thesis |

| Direct Stocks | Tactical | High conviction, time-bound, thesis-driven |

| Liquid / Arbitrage Fund | Tactical | Parking tactical dry powder before deployment |

Mid and small-cap funds are the most misclassified investments in Indian portfolios.

Investors buy them tactically during a rally but hold them like Core when they fall — the worst of both worlds.

Where This Sits in the RSW Financial Independence Framework

The RSW Financial Independence Framework identifies five stages of wealth building for salaried professionals.

Core and Tactical allocation plays a different role at each stage.

In the early accumulation stage, almost everything should be Core. You are building the foundation.

The Tactical layer, if any, should be minimal — you do not have enough corpus to absorb a wrong call.

In the growth stage, a modest Tactical layer (15 to 20%) makes sense.

You have a meaningful corpus, a clearer risk profile, and enough financial cushion to take calculated short-term positions.

In the pre-independence stage, the Core becomes increasingly non-negotiable.

Capital preservation takes priority. Tactical positions, if taken, should be defensive in nature — not return-enhancing.

[Explore the full RSW Framework →]

The Salaried Professional Reality

The Core-Tactical framework was originally designed for institutional investors and high-net-worth portfolios. Applying it to a salaried professional context requires one important adjustment:

Simplicity of execution.

You do not have a portfolio manager monitoring your positions daily.

You have a job, a family, and perhaps two hours a month you can give to your finances. This means:

Your Core must be largely automated — SIPs into index funds, large-cap funds, or a balanced advantage fund that does the rebalancing for you.

Your Tactical layer must have hard limits — both in size and in the number of positions.

One or two tactical calls at a time, maximum. If you cannot clearly articulate the thesis in two sentences, you should not be making the move.

And critically — in India, every tactical move has a tax cost.

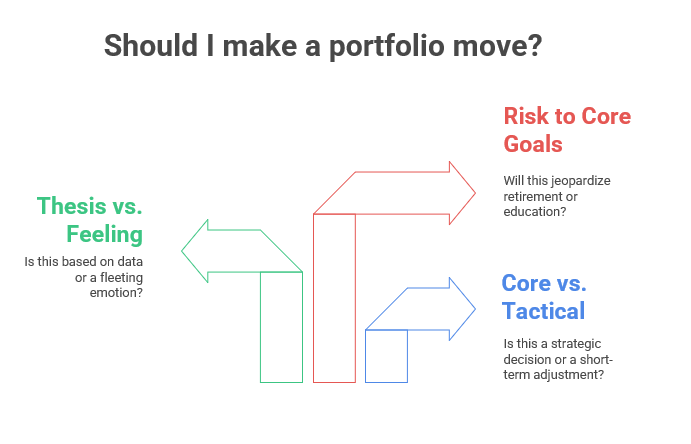

Three Questions Before You Make Any Portfolio Move

Before touching your portfolio — for any reason — ask yourself these three questions:

- Is this a Core decision or a Tactical decision? If you cannot answer this clearly, stop.

- Am I acting on a thesis or a feeling? A thesis has data behind it. A feeling has a market headline behind it.

- If this move goes wrong, which goal does it put at risk? If the answer is any of your Core goals — retirement, education, financial independence — the move should not happen.

These three questions will not make you a perfect investor. But they will stop you from making the decisions that do the most damage.

The Architecture Is the Strategy

Core and Tactical allocation is not a sophisticated concept reserved for wealthy investors or financial experts. It is a simple structural decision that every salaried professional can and should make.

A portfolio without a Core drifts with every market cycle.

A portfolio without any Tactical flexibility creates pressure that eventually leads to impulsive decisions. The two-bucket architecture keeps both failure modes in check.

The goal is not to build a perfect portfolio. The goal is to build one you can stay with — through bull markets, corrections, rate cycles, and every headline that tells you to do something different.

That is what Core and Tactical allocation, applied with discipline, makes possible.

The RSW Framework at persfinanceplanning.in applies Core and Tactical thinking across all five stages of wealth building — helping salaried professionals build portfolios that are both resilient and responsive. [Start here →]

Your portfolio will drift. The market guarantees it. What you choose to do about it — and when — is the only variable within your control.

Begin your rebalancing review for you Portfolio [ Book a Call ] →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”