The R.S.W. Financial Independence Framework — A Complete Guide

Most salaried professionals in India are not bad at earning. They are bad at structuring.

They invest, insure, buy property, open NPS accounts.

But each of these decisions lives in isolation — disconnected from a purpose, detached from a sequence, and unconnected from one another.

The result is a portfolio that looks active but functions passively.

If you are between 30 and 50, earning a decent income, and still unable to clearly answer these three questions —

- What is my retirement corpus, and am I on track?

- Is my family protected if I am not around tomorrow?

- Are my investments aligned to actual goals, or just performing?

— then what you need is not a better mutual fund. You need a framework.

The R.S.W. Financial Independence Framework is a structured, five-stage wealth planning system built exclusively for salaried professionals.

It does not chase returns. It builds sequence — converting income into a system where managing money comes first, protection comes second, and growth follows only when the foundation is ready.

This page is the map. Every guide, tool, and deep-dive on this website connects back to one of its five stages.

Who This Framework Is Designed For

The R.S.W. Financial Independence Framework is built for:

- Salaried professionals aged 30 to 50 in India

- Dual-income households managing competing goals

- Families planning for children’s higher education or marriage

- Individuals serious about quantifying and reaching retirement readiness

- Investors who want structure and direction — not just returns

It is not for speculative traders seeking short-term gains. It is for disciplined wealth builders who want a system — and the clarity to know exactly where they stand within it.

Why Salaried Professionals Need a Structured Framework

A salary is not the same as wealth. It is the raw material.

Your earning window is finite. Expenses will rise — lifestyle, education, healthcare. Retirement will arrive whether you plan for it or not. And unlike a business owner, you cannot extend your earning years indefinitely or liquidate equity to fund a cash crunch.

This creates a fundamental challenge: salaried wealth is entirely dependent on how surplus income is allocated over time.

Without structure, this is what typically happens:

- Insurance is bought for the wrong reasons, in the wrong form, at the wrong coverage.

- Investments are made in response to market news, not in service of goals.

- A retirement corpus is never actually calculated — it is hoped for.

- The portfolio grows — but grows without a plan.

A structured framework fixes the sequence. It ensures that every rupee you allocate has a designated job: managing your money first, building a safety net second, and only then investing for goals and growth.

The single biggest mistake salaried investors make is not a bad investment — it is investing before the foundation is ready.

→ Read: Why Holistic Wealth Management Never Crosses the Indian Mind

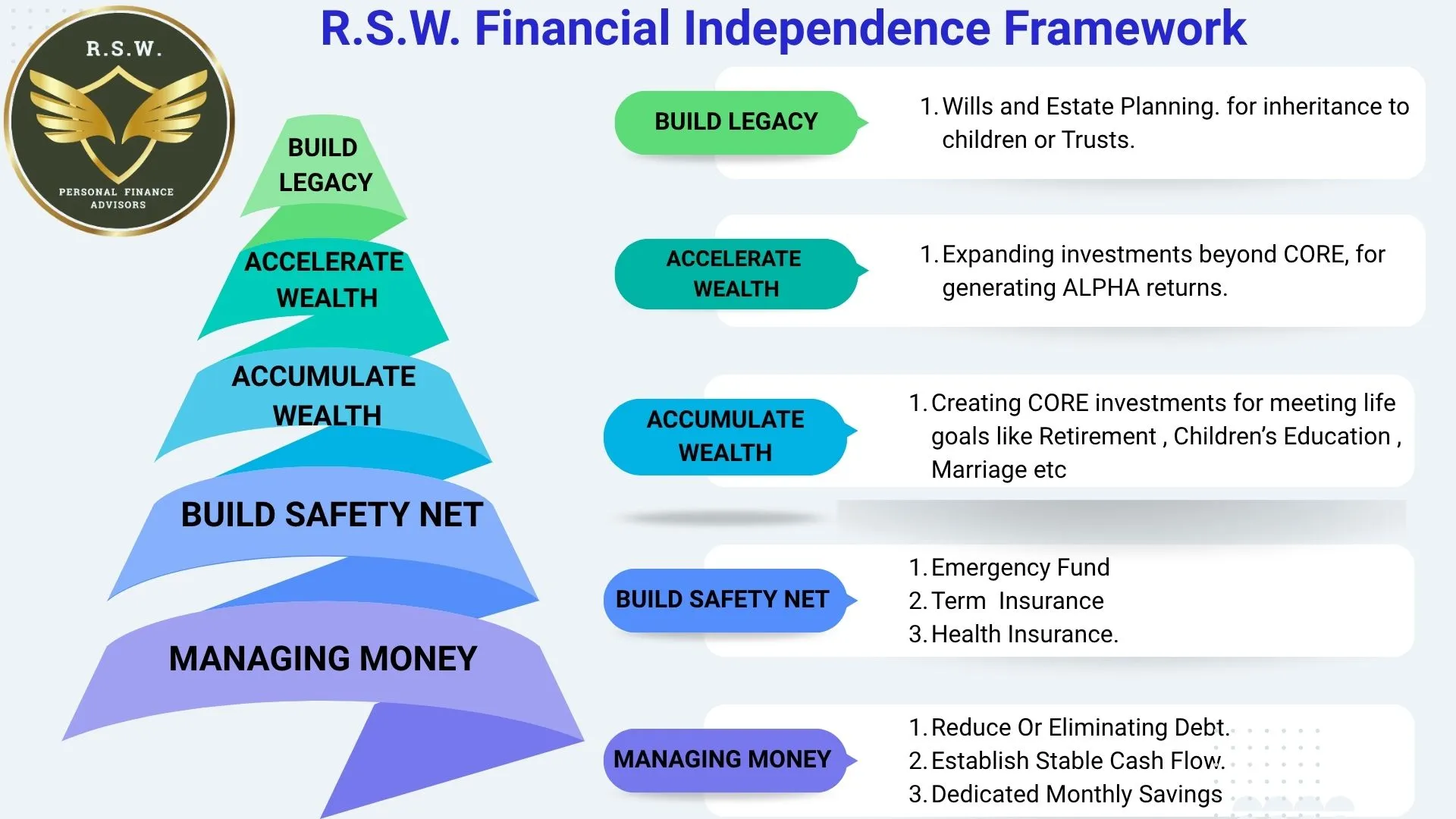

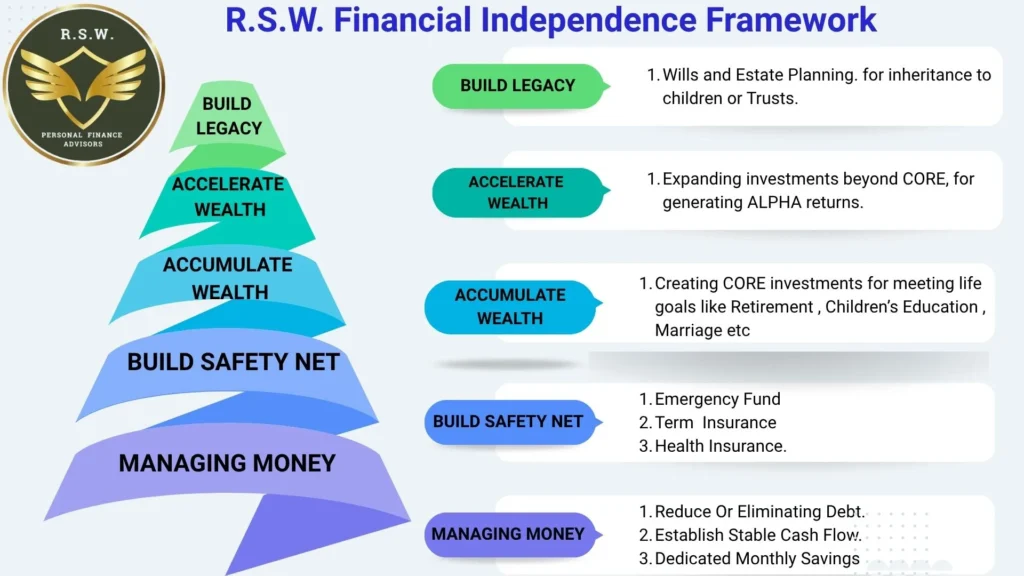

The 5-Stage R.S.W. Framework at a Glance

The R.S.W. Financial Independence Framework is not a checklist.

It is a sequence. Each stage creates the conditions for the next to function.

| Stage | Name | What It Does |

|---|---|---|

| Stage 1 | Managing Money | Reduce or eliminate debt · Establish stable cash flow · Dedicated monthly savings |

| Stage 2 | Build Safety Net | Emergency fund · Term insurance · Health insurance |

| Stage 3 | Accumulate Wealth | CORE investments for life goals — retirement, children’s education, marriage |

| Stage 4 | Accelerate Wealth | Expand beyond CORE with Tactical investments to generate Alpha returns |

| Stage 5 | Build Legacy | Wills, estate planning, inheritance to children or trusts |

Where Are You Right Now?

Most salaried investors are somewhere between Stage 2 and Stage 4 — but with gaps they are not aware of. Use this to locate yourself before reading further.

| If this describes you | You are here | Start here |

|---|---|---|

| Have SIPs running but no emergency fund or term cover | Stage 2 incomplete | Read Stage 2 first |

| Carrying a personal loan while also investing | Stage 1 unfinished | Read Stage 1 first |

| Have insurance and emergency fund but investing without goal targets | Stage 3 — but without CORE structure | Read Stage 3 carefully |

| Have a CORE portfolio but surplus capital with no clear strategy | Ready for Stage 4 | Read Stage 4 |

| Have not thought about nominations, wills, or estate planning | Stage 5 unaddressed | Read Stage 5 |

The framework’s job is to identify the gaps and sequence the fixes.

1. Managing Money

Control precedes capital.

Before a single investment is made, three things must be in order: your debt, your cash flow, and your savings habit. This is not a budgeting exercise. It is the structural foundation on which every other stage depends.

1. Reduce or Eliminate Debt

Not all debt is the same. There are two categories, and the distinction matters.

Debt for asset creation is a tool. A home loan borrows to acquire something that appreciates, generates equity, and serves a life goal. This kind of debt is not just acceptable — it is often the right decision.

Debt for consumption is a drain. A car loan finances a depreciating asset. A credit card balance finances spending that has already happened. A personal loan finances nothing at all — there is no asset behind it, no income it generates, only a monthly outflow consuming surplus that should be building a future.

Personal loans deserve the sharpest focus. They are the most corrosive form of consumer debt a salaried professional can carry. If you have one, closing it is not a goal — it is a financial emergency. Every rupee directed toward it earns a guaranteed return equal to the interest rate being charged. No investment competes with that certainty.

Map every liability. Manage asset-creation debt. Eliminate consumption debt systematically. Close personal loans first, with fierce focus.

Only then does surplus flow cleanly into Stage 2 and beyond.

2. Establish Stable Cash Flow

Most salaried professionals significantly underestimate their actual monthly outflows — the sum of fixed expenses, discretionary spending, EMIs, insurance premiums, and irregular annual costs averaged across 12 months.

Stable cash flow does not mean cutting spending. It means knowing, with clarity, exactly what comes in and what goes out — and ensuring the gap is real, consistent, and growing.

3. Dedicated Monthly Savings

Wealth is not built from what is left after spending. It is built by automating what is set aside first. Stage 1 ends with a fixed monthly savings number — non-negotiable, automated, and flowing into Stage 2 before any discretionary spending occurs.

If monthly surplus is unstable or undefined, every investment decision downstream is built on sand.

2. Build Safety Net

If the foundation cracks, everything above it falls.

This is the most under-engineered stage in most salaried investors’ plans. It is also the one that determines whether the rest of the framework survives a life event — a job loss, a medical emergency, or the death of the income earner.

Stage 2 has three components. All three are non-negotiable.

1. Emergency Fund

A liquid reserve of 6 to 8 months of total household expenses — not salary, not income, but actual outflows including EMIs, education fees, and insurance premiums.

This fund does not sit in a savings account earning 3%. It sits in instruments that are instantly accessible and do not depreciate — liquid mutual funds, sweep-in FDs, or ultra-short-duration debt funds.

The emergency fund protects your goal-linked investment portfolio — what the R.S.W. framework calls your CORE — from being dismantled the moment life does not go to plan.

→ Read: Emergency Fund: Where Should You Park It? https://persfinanceplanning.in/where-to-park-emergency-fund/

2. Term Insurance

This is the single most important financial product for a salaried professional with defendants and liabilities.

If your income disappears tomorrow, does your family’s financial plan survive?

Term cover must be sized to:

- Clear all outstanding liabilities (home loan, personal loans)

- Replace income for dependants over the required number of years (typically 10–15x annual income)

- Cover the timeline until the family reaches financial independence — not just retirement age

An employer’s group cover is not a substitute. It ends when employment ends.

→ Read: Why Term Insurance Is the First Step Towards Wealth Planning https://persfinanceplanning.in/why-term-insurance-first-step-wealth-planning/

3. Health Insurance

A medical event without adequate cover can dismantle a decade of disciplined investment in weeks. Employer-provided health cover has limits, portability issues, and no continuity after employment. A personal, family floater policy — independent of your employer — is the correct structure.

Risk protection does not generate returns. But it protects every rupee that compounding is building. Without Stage 2, the framework is fragile. With it, it is resilient.

3. Accumulate Wealth

Every rupee must have a goal. But first — what exactly is a CORE investment?

Consider a 38-year-old professional with a stable income, a home loan, two children, and a rough idea that retirement is “something to plan for later.” They have three SIPs running — chosen because a friend recommended them, have an NPS account opened for the 80C benefit. They have an LIC policy bought at their mother’s insistence.

None of these is wrong. But none of them is a CORE. Because no one has ever linked any of them to a specific goal, calculated the corpus required, or built a rebalancing schedule behind them.

That is the gap Stage 3 closes.

Most salaried investors have a portfolio. Very few have a CORE.

The difference is not in the instruments they hold. It is in the purpose behind each one.

In the R.S.W. framework, CORE investments are defined precisely — not by what they are called, but by what they are built to do.

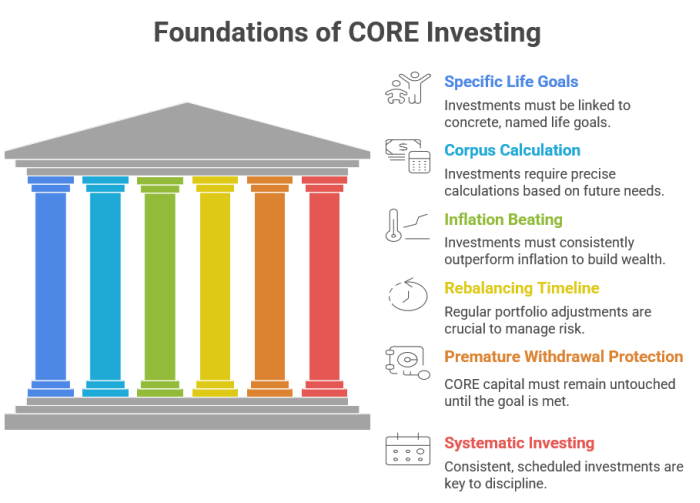

A CORE investment must satisfy all six of the following characteristics:

1. It is linked to a specific, named life goal.

Retirement. A child’s college fees. A home purchase. A daughter’s marriage. Not “long-term wealth” in the abstract — a specific goal with a specific target date and a calculated corpus. If you cannot answer “which goal does this investment fund?” — it does not belong in the CORE.

2. It is backed by a corpus calculation.

The SIP amount, the asset class, and the investment duration are all derived from a number — the inflation-adjusted amount needed at a specific future date. Without that calculation, it is a guess dressed as a plan.

3. It must consistently beat inflation.

An investment that fails to outpace inflation is not building wealth — it is slowly eroding it, while appearing to grow. India’s long-run inflation runs at 6–7% annually. A CORE investment must, over its full duration, deliver real returns above this threshold. This is why fixed deposits, savings accounts, and traditional insurance-linked products — however comfortable they feel — cannot anchor a CORE portfolio. Comfort that does not outpace inflation is a quiet, long-term loss.

4. It has a defined rebalancing timeline.

A CORE portfolio does not run on autopilot indefinitely. Markets move. Asset allocation drifts. An equity-heavy portfolio built for a 15-year horizon becomes inappropriately risky if left untouched as the goal approaches. Every CORE investment must come with a predetermined rebalancing schedule — typically an annual review — and a horizon-based de-risking plan that shifts allocation progressively from growth to stability in the final 3–5 years before the goal falls due. Without this schedule, the CORE becomes a neglected portfolio, not a managed one.

5. It is protected from premature withdrawal.

CORE capital is ring-fenced. It is not redeemed when the market falls, not touched for a vacation or a car upgrade, and not redirected toward a new opportunity. Its only legitimate exit is the goal it was built for. The CORE’s power comes from uninterrupted compounding — every premature withdrawal resets a portion of the clock.

6. It is systematic and ongoing — not event-driven.

CORE investing runs on a schedule. SIPs debit on the same date every month regardless of market level or sentiment. The decision to invest is made once, at the point of goal-setting. After that, the system runs without interference. Event-driven investing — adding money when markets feel good, pausing when they don’t — is the opposite of CORE discipline.

CORE Investment Classification

The table below identifies which instruments qualify as CORE in the R.S.W. framework, and why. Each instrument links to a dedicated guide on this website.

| Investment Option | Why It Is CORE |

|---|---|

| Nifty 50 / Sensex Index Fund | Broad market, low cost, long-term compounder |

| Large-cap Mutual Fund | Stable, diversified, goal-aligned |

| PPF / EPF / SSY | Tax-efficient, long-duration, non-negotiable |

| NPS — National Pension System | Tax-efficient, lock-in enforces discipline, retirement-specific |

| Term Insurance | Protection layer — not an investment, but foundational to every CORE plan |

| Balanced Advantage Fund | Built-in rebalancing, suits passive investors |

| Flexi Cap / Multi Cap Fund | Equity diversification across market caps, long-horizon compounder |

| Debt Mutual Fund — Long Duration | Stability and income over 3+ year horizon |

| Real Estate — Self-occupied | Long-duration asset, goal-linked |

| Mid-cap / Small-cap Fund — via SIP, 7+ years | Core when held systematically over long duration; Tactical if deployed as lump sum on correction |

The instrument alone does not make something CORE. The intent, the discipline, the goal-linkage, and the rebalancing commitment behind it do.

What Does Not Belong in the CORE

| Investment | Classification | Reason |

| Thematic fund bought because a sector is trending | Tactical, not CORE | No named goal, no corpus calculation — thesis-driven, not goal-driven |

| FD rolled over out of habit | Not CORE | Not goal-linked, does not reliably beat inflation, no rebalancing plan |

| NPS account opened only for the 80C deduction | Becomes CORE only when… | …linked to a retirement corpus calculation, held with discipline, and reviewed annually |

| Smallcase or direct stock position opened out of curiosity | Tactical — belongs in Stage 4 | No systematic commitment, no goal-linkage, thesis-driven entry and exit |

The CORE is not defined by what you invest in. It is defined by why, how systematically, and how purposefully you invest.

4 Accelerate Wealth

Growth beyond CORE. Alpha beyond safety.

Most salaried investors attempt Stage 4 prematurely — before the CORE is built, before goals are funded, before protection is in place. That is not acceleration. That is speculation on an unfinished foundation.

Stage 4 begins only when your CORE portfolio is structured, on track, and self-sustaining. At that point, additional investable capacity — surplus beyond what the CORE requires — can be deployed with a longer horizon and higher risk tolerance, specifically to generate Alpha: returns above what the CORE alone can deliver.

The instruments in Stage 4 are Tactical by nature. They carry a time-bound thesis, a defined entry rationale, and an exit plan. not held indefinitely, not goal-linked in the same way CORE investments are. They are positioned to capture specific opportunities — sectoral momentum, macro themes, currency diversification, or market corrections.

Tactical Investment Classification

The table below identifies which instruments belong in the Tactical layer of Stage 4, and why. Each instrument links to a dedicated guide on this website.

| Investment Option | Why It Is Tactical |

|---|---|

| Sector / Thematic Fund | Time-bound thesis, high concentration risk |

| Gold ETF | Short-term positioning on macro or geopolitical thesis |

| International Fund / ETF | Currency and global diversification play, time-bound |

| Smallcases | Curated, strategy-driven equity baskets — thematic or factor-based, with a defined thesis |

| Short Duration Debt Fund | Interest rate cycle positioning |

| Real Estate — Rental / Commercial | Opportunistic entry, income-generating thesis |

| Direct Stocks | High conviction, time-bound, thesis-driven |

| Liquid / Arbitrage Fund | Parking tactical dry powder before deployment |

| Mid-cap / Small-cap Fund — lump sum on correction | Tactical when deployed as lump sum with defined exit; CORE when held via SIP over 7+ years |

Tactical investments are not better or worse than CORE investments. They serve a different purpose — and require a different level of active management, thesis clarity, and exit discipline.

The Boundary Between CORE and TACTICAL

One instrument spans both categories: Mid-cap and Small-cap Funds. The instrument is identical. The classification depends entirely on how it is used.

Held via SIP over 7 or more years — goal-linked, systematically invested, with a rebalancing plan — it is CORE. The long duration absorbs volatility and gives compounding room to work.

Deployed as a lump sum on a market correction — with a thesis, a target return, and a defined exit — it is Tactical. It belongs in Stage 4, managed as Alpha capital, not CORE capital.

The intent, the duration, and the discipline around it determine the classification. Not the fund itself.

→ Read: Smallcase Investing: Where It Fits in a Modern Wealth Strategy

→ Read: The Portfolio Blind Spot Most Indian Investors Don’t Know They Have

In the R.S.W. framework, Accelerate Wealth is not the starting point. It is the reward for completing the foundation.

5. Build Legacy

Financial independence does not end at retirement. It must continue beyond you.

Wealth that is not structured for transfer is wealth that will be lost — to legal disputes, inefficient taxation, family conflict, or simply the absence of a clear written plan.

Most salaried professionals spend decades building wealth and almost no time structuring what happens to it. The assumption is that this can be addressed “later” — after retirement, after the children settle, after things slow down. It rarely happens.

And when it doesn’t, the consequences fall entirely on the people you spent your life building the wealth for. A missing nomination. An unregistered will. Assets held jointly without a clear succession plan. These are not rare edge cases — they are the norm in most Indian households. Stage 5 exists to make sure your plan survives you.

Stage 5 extends the framework beyond your working years and into the generation that follows. It converts personal wealth accumulation into generational continuity.

Build Legacy Includes:

Wills and Estate Planning

A legally valid will is the minimum. It specifies asset distribution clearly and unambiguously — preventing disputes and ensuring your intentions are legally enforceable. Without a will, the law decides. That is rarely what you would have chosen.

Nomination Review

Nominees on every financial instrument — mutual funds, insurance policies, bank accounts, NPS, EPF — must be reviewed and aligned to current intent. Outdated nominations are one of the most common and most costly oversights in Indian households.

Inheritance to Children or Trusts

For larger estates, or where specific conditions around inheritance matter — minor children, dependants with special needs, staged distribution over time — a trust structure offers control over how and when wealth passes to the next generation.

Tax-Efficient Transfer

Structuring asset transfer to minimise tax implications for beneficiaries is the final act of disciplined wealth planning — ensuring that what took decades to build is not diminished at the point of transfer.

A wealth plan without a legacy structure is a plan that ends at death. A complete plan continues beyond it.

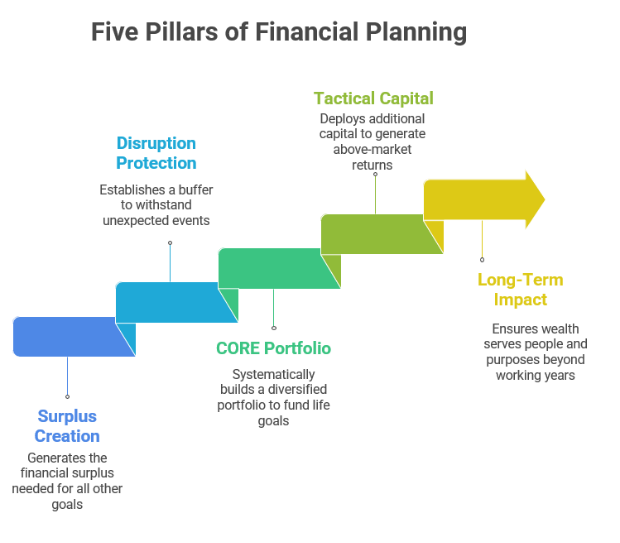

How the R.S.W. Framework Creates Financial Independence

Financial independence is not a feeling of comfort. It is a funded structure — built deliberately, in sequence, over time.

The five stages work together:

- Managing Money creates the surplus that makes everything else possible.

- Building a Safety Net ensures the plan survives disruption.

- Accumulating Wealth converts surplus into a CORE portfolio that funds every major life goal — systematically, inflation-beating, and rebalanced on schedule.

The R.S.W. Financial Independence Framework achieves this through one principle above all others: sequence.

Managing Money comes before Building a Safety Net. Safety Net comes before Accumulating Wealth. Accumulating Wealth comes before Accelerating Wealth. Accelerating Wealth comes before Building Legacy.

Each stage builds resilience. Resilience sustains compounding. Compounding builds wealth. Structured wealth, in sequence, becomes independence.

Your Next Step

You now have the map.

The question is: where are you on it?

You may have insurance that has not been reviewed since it was bought. A goal that exists as an intention but not as a calculated corpus. A portfolio accelerating into Alpha before the CORE is even properly structured.

A single, focused conversation is enough to locate you in the framework, identify the gaps, and build a clear sequence of what to prioritise next.

No sales pitch. No products pushed. Just an honest map of where you stand.

Book your free one-hour wealth planning call →

Nitin Wali is the founder of R.S.W. Personal Finance Advisors, a Pune-based Chartered Wealth Manager (CWM), AMFI-registered Mutual Fund Distributor (ARN–244802), and registered PMS Distributor (APRN07002). All content on this website is for educational purposes only and does not constitute investment advisory services under SEBI (Investment Advisers) Regulations.

| Stage | Deep Dive Articles |

|---|---|

| Managing Money | Why Holistic Wealth Management Never Crosses the Indian Mind |

| StaBuild Safety Net | Emergency Fund: Where Should You Park It? · Why Term Insurance Is the First Step Towards Wealth Planning |

| Accumulate Wealth (CORE) | Comprehensive Guide to Equity Mutual Funds · ETF Investing India · Best Flexi Cap Funds · NPS Returns in India · NPS: Beyond Returns & Rankings · NPS: A Complete Guide to Retirement Planning · Cooperative Credit Society Deposits Core and Tactical Allocation |

| Accelerate Wealth (TACTICAL) | Smallcase Investing: Where It Fits in a Modern Wealth Strategy · The Portfolio Blind Spot Most Indian Investors Don’t Know They Have |

| Build Legacy | Articles coming soon |

Book your free one-hour wealth planning call →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”