I’ll be honest — I almost didn’t write this article.

Not because the topic isn’t important. It’s probably the most important thing I could write about. But because I know how it’s going to land for a lot of people reading it.

Uncomfortable.

Maybe a little personal.

Possibly even annoying.

Good.

That’s exactly the point.

Morgan Housel’s Psychology of Money sits on more Indian bookshelves than almost any finance book of the last decade.

Parag Parikh spent thirty years telling Indian investors the truth about their own behaviour — overconfidence, herd mentality, chasing tips, refusing to be patient.

Both of them were right. Both of them did important work.

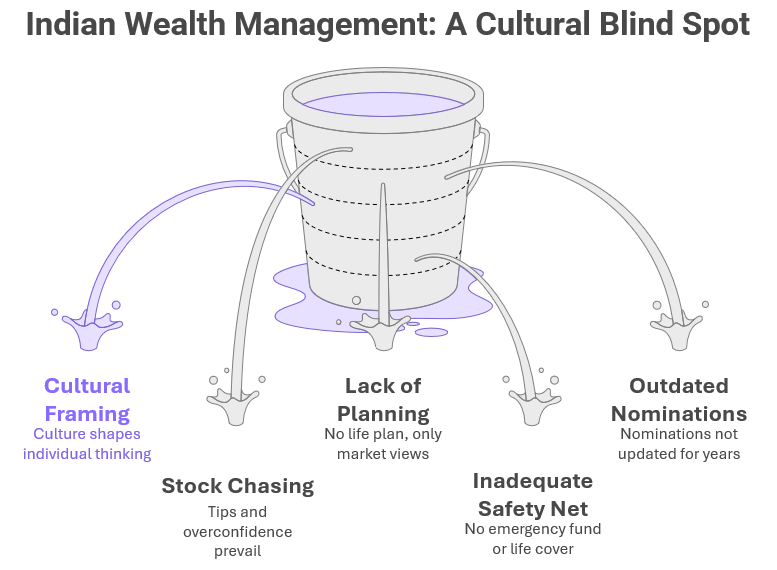

And yet — when I sit across from a 42-year-old software engineer in Pune who has three SIPs running, follows six stock market influencers on YouTube, and can tell me the P/E ratio of his favourite mid cap fund — I still have to ask him gently whether his family would be financially okay if something happened to him tomorrow.

The silence that follows that question is the whole article.

The Hunter Has Entered the Chat

Here’s something neither Housel nor Parikh quite said directly: the problem isn’t just psychological. It’s primal.

Evolutionary psychology tells us the male brain is wired — disproportionately, persistently — for the hunt.

The chase.

The catch.

The return to camp with something to show the others.

Two hundred thousand years of that wiring doesn’t disappear because we now have demat accounts instead of spears.

Watch how the typical Indian salaried male — educated, 35 to 50, earning well — actually engages with his money.

He’s animated by the next IPO.

Tracks his portfolio on his phone during lunch.

Forwards multibagger tips on WhatsApp at 11pm with the energy of someone who’s just discovered fire.

Feels a genuine, warm pride when he can mention at a family dinner that he got into a particular stock before everyone else did.

Now ask him about his term insurance cover.

Silence.

Ask him when he last looked at his emergency fund.

Vague deflection. Something about “I have some savings.”

Ask him whether his nominations across his mutual funds, his EPF, his bank accounts — are they actually updated after his father passed away two years ago?

Discomfort.

A subject change.

The chase feels like living. The tending feels like admin.

And that feeling — not ignorance, not laziness, but that visceral difference in how each one feels — is why holistic wealth management never even gets thought about, let alone acted on.

What Housel and Parikh Both Missed

Housel tells you to think long-term. Compounding is magic.

Wealth is what you don’t spend. All of it true, all of it worth reading.

But Housel wrote from Seattle. His frame is individual psychology — how you, as a person, think about money.

What he didn’t reckon with is how culture sets the frame before the individual even shows up.

Parikh understood the Indian investor deeply. He saw the stock-chasing, the tips-following, the overconfidence. He spent his career trying to redirect that energy toward patience and value.

But here’s the gap in both their arguments — and I say this with genuine respect for both:

Neither of them asked why the Indian mind reduces all of wealth management to investing in the first place.

I’ve met men with no emergency fund, dangerously inadequate life cover, nominations that haven’t been updated in a decade, and no clarity on what their money is actually supposed to do for their family — who will still tell you, with complete confidence, that they “manage their finances well.”

Because in the Indian context, managing finances means having views on the market. Not having a plan for your life.

That plan has a name — and a structure. The RSW Financial Independence Framework

The Dinner Table Test

This is the part of the article I debated cutting. It’s a little uncomfortable to write. But I think it’s the most important bit.

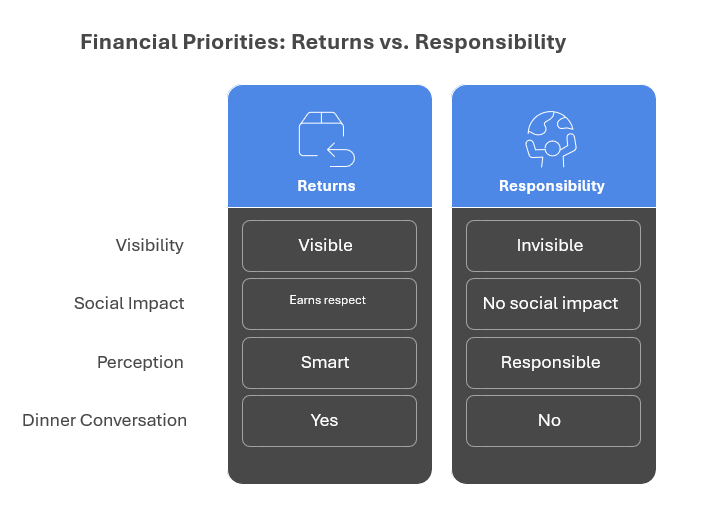

At family dinners, at office conversations, at building society meetings — the question that earns genuine respect among Indian men is not “do you have a complete financial plan?”

It is “kitna return mila?”

Return is visible. It’s a number. You can say it out loud and watch people’s faces change.

A well-structured financial life — adequate term cover, a funded emergency reserve, goal-based investments, updated nominations, a drafted will — is completely invisible.

It doesn’t come up at dinner. There’s no number to quote. No story to tell.

And so, slowly, over years of social reinforcement, a man’s financial identity gets built around his portfolio.

The portfolio becomes a proxy for how smart he is.

A multibagger in the portfolio means you know things. A term plan and an emergency fund mean you’re merely… responsible.

Responsible doesn’t get you respect at the dinner table. Returns do.

The Silent Cost of Looking Financially Smart

I’ve watched this dynamic play out in client conversations more times than I can count. It’s not about ego exactly. It’s about what we’ve been taught — implicitly, repeatedly — that financial competence looks like.

And what it looks like is a winning trade, not a complete plan.

That conditioning is more powerful than any cognitive bias Kahneman ever described. Because it’s not just internal. It’s social. It’s daily.

And it comes from people you respect.

Boring Is Actually the Feature

The financial content industry — finfluencers, YouTube channels, financial news — will never tell you this. Because it kills their business model.

Holistic wealth management is boring by design.

Not because it’s unimportant. Because it’s so foundational that it works quietly, in the background, without needing your daily attention. That’s the whole point.

An emergency fund just sits there. Doing nothing interesting. Until the month you lose your job and your family doesn’t have to borrow at 18% interest to pay school fees.

The Plan That Works While You Are Not Watching

Term insurance costs you money every single year with zero visible return. Until it pays your family ₹1.5 crore when you’re no longer around — and at that point, whether the cover was adequate or not is a conversation nobody gets to have with you.

A written financial plan gives you nothing to track on a daily basis. No excitement. No alert to screenshot and forward.

Just a framework — a way to evaluate every financial decision against where your life is actually going, not where the Sensex is going tomorrow.

The hunter in you will find none of this interesting.

That’s not a bug. That’s precisely what makes it work.

So — Are You Hunting or Building?

The Indian salaried professional isn’t financially illiterate. He is financially selective.

He goes deep on the parts of personal finance that feel like hunting — stock research, fund comparisons, return calculations. Systematically avoids the parts that feel like tending.

And that selectivity — not bad luck, not market timing, not the wrong fund choice — is the single biggest threat to his financial future.

Patience Is Not Enough

Parag Parikh spent years trying to make Indian hunters into patient equity investors. He was right that patience matters. But patience within a single asset class is still hunting — just slower.

A complete financial life also requires you to tend — to review, to rebalance your portfolio, to protect what you’ve built before you’ve finished building it.

Housel was right that financial success is about behaviour. But the behaviour that matters most in the Indian context isn’t just how you invest. It’s whether you’ve decided — actually decided — to build a financial life. All of it. Together. As one system that holds.

I’ll leave you with the only question this article was really asking.

When you look at your financial life right now — honestly, not optimistically — are you hunting?

Or are you building?

Because those aren’t the same thing. They never were. And no return, no multibagger, no perfectly timed IPO allotment will close the gap between them.

The RSW Financial Independence Framework at persfinanceplanning.in applies Core and Tactical thinking across all five stages of wealth building — helping salaried professionals build portfolios that are both resilient and responsive. [Start here →]

If that question stayed with you — you already know the answer.

Let’s have an honest conversation about where you actually stand.

No pitch. No pressure. Just clarity.

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”