You have built a solid SIP in an Indian equity fund. Your portfolio is growing. You review it every year and feel in control.

But here is a question worth sitting with.

100% of your investment growth depends on what happens to the Indian economy.

If Indian markets underperform for a decade — and they have, in certain periods — your entire wealth-building plan slows down with it. Not because you made a poor choice.

Because you concentrated everything in one geography.

This is not a criticism of Indian markets. India remains one of the most compelling long-term investment stories in the world.

But concentration — even in a good story — is a risk. Structured investors manage it deliberately.

International investing is how you manage it.

Why Bother? The Case for Going Global

Here is why international investing earns a place in a structured portfolio.

1 . The numbers make the case

Look at this table of global equity market returns in USD, as of February 28, 2026: [ *CAGR]

| Market | 1-Year* | 3-Year* | 5-Year* | 10-Year* |

|---|---|---|---|---|

| South Korea | 182% | 40% | 14% | 15% |

| Brazil | 70% | 20% | 12% | 12% |

| Vietnam | 61% | 22% | 3% | 5% |

| Japan | 41% | 22% | 9% | 10% |

| Emerging Markets | 34% | 17% | 5% | 10% |

| Europe | 32% | 18% | 11% | 11% |

| World Index (ACWI) | 24% | 21% | 12% | 13% |

| US (S&P 500) | 17% | 22% | 14% | 15% |

| China | 13% | 10% | −5% | 6% |

| India (Nifty) | 2.5% | 8% | 6% | 9% |

India’s 1-year USD return of 2.5% is among the weakest globally.

South Korea’s 182% one-year run reflects an AI and semiconductor re-rating.

A pure India portfolio has significantly underperformed a diversified global one over the past year.

No single geography dominates every decade.

Spreading across geographies reduces the damage when one country underperforms.

2 : Access to companies you cannot buy through Indian funds

Apple. Microsoft. Amazon. NVIDIA. Alphabet.

None of these are listed on Indian exchanges.

Between January and March 2026 alone, these five companies — along with Meta and Oracle — collectively committed $690 billion in capital expenditure towards AI infrastructure.

Nvidia’s data centre business clocked $62.3 billion in a single quarter.

If you invest only in Indian equity funds, you have zero exposure to this. International investing gives you access to businesses and innovation cycles that do not exist in the Indian listed space.

3 : Currency as a natural hedge

The rupee has weakened against the dollar over the long term. When it does, your international investments — held in foreign currencies — become more valuable in rupee terms.

This is not speculation. It is a structural benefit that compounds quietly over time.

4 : Behavioural stability

BlackRock’s Chief APAC and Middle East Strategist put it plainly: “Diversification is the only free lunch in a crisis.”

In calm markets, a single-country portfolio works fine. In stress, you need more options. A geographically diversified portfolio reduces the emotional pressure to exit at exactly the wrong moment.

What Does “Investing Internationally” Actually Mean?

Most people hear “international investing” and imagine complexity. Foreign brokerage accounts. Currency conversions. Overseas wire transfers. Tax nightmares.

The reality for an Indian investor today is far simpler.

Do not need a foreign bank account.

No need to understand how to trade on the New York Stock Exchange.

You do not need to convert ₹ to $ before you invest.

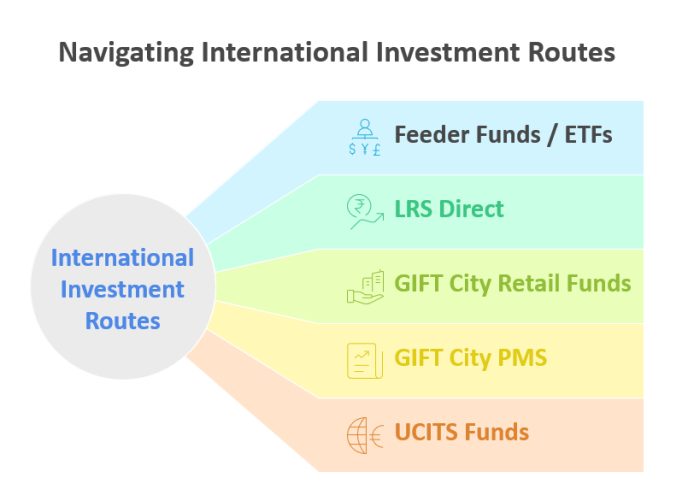

There are five distinct routes available to Indian residents. Each works differently. Each has its own cost, tax treatment, and minimum. Understanding the map is the first step.

The Five Routes to International Markets

Route | How It Works | Annual Limit | Tax [ LTCG ] | Minimum |

|---|---|---|---|---|

| Feeder Funds / ETFs | Domestic AMC invests overseas on your behalf | Subject to RBI/SEBI cap | 12.5% | ₹500 SIP |

| LRS Direct | You invest via foreign brokers (Vested, IBKR, INDmoney) | $250,000/year | 12.5% | Varies |

| GIFT City Retail Funds | Funds domiciled in IFSC; not subject to SEBI overseas cap | No RBI cap | 14.95% (after 24 months) | $5,000 |

| GIFT City PMS | Portfolio Management Services in IFSC | No RBI cap | 20% (after 24 months) | $150,000 |

| UCITS Funds | European-domiciled funds; primarily for NRIs in UK/Europe | Varies by country | Varies | Varies |

For most salaried professionals building wealth in India, Routes 1 and 2 are the natural starting points. GIFT City becomes relevant as portfolio size grows.

UCITS is primarily relevant if you live or work abroad.

Feeder Funds and International ETFs

These are the most accessible entry points. Both are SEBI-regulated, rupee-denominated, and available through your existing investment account or demat.

International Mutual Funds — What They Are and How They Work

An international mutual fund is a SEBI-registered fund that invests in overseas markets on your behalf.

The fund pools money from Indian investors and uses it to buy international stocks, bonds, or units of overseas funds.

There are two main structures.

Fund of Funds (FoF)

A Fund of Funds does not buy international stocks directly. It invests in an existing overseas mutual fund — typically from a global asset manager like Franklin Templeton, Vanguard, or BlackRock.

Your ₹ → Indian FoF → Overseas Fund → International Stocks.

As an Indian investor, you buy units in rupees. The Indian fund converts and invests in the underlying overseas fund. You never handle a foreign currency.

Directly Investing International Funds

Some Indian mutual funds invest directly into international stocks — without routing through another fund. These tend to be thematic. Global technology. Healthcare. Consumer brands.

Either way, your experience as an investor mirrors any domestic mutual fund.

Invest in rupees.

Receive units in your folio.

You check your NAV daily.

One important regulatory constraint

In early 2022, SEBI imposed an industry-wide limit on how much Indian fund houses can collectively invest overseas — $7 billion across all AMCs. This limit was breached. Most international fund of funds paused fresh lump sum subscriptions.

Some AMCs have since resumed, within their individual limits. The situation remains fluid. Before investing in any international mutual fund, verify with your advisor or the AMC directly whether the scheme is currently accepting fresh investments.

International ETFs — What They Are and How They Work

An ETF — Exchange Traded Fund — is a fund that tracks an index and trades on a stock exchange like a share.

An international ETF listed on Indian exchanges tracks an international index. The S&P 500. The Nasdaq 100. The Hang Seng.

You buy units through your demat account — the same way you would buy a share of Infosys or Reliance. The price moves in real time during market hours.

Examples of International ETFs listed in India:

- Motilal Oswal S&P 500 ETF

- Motilal Oswal Nasdaq 100 ETF

- Nippon India ETF Hang Seng BeES

- Mirae Asset NYSE FANG+ ETF

These are available on BSE and NSE. Most demat accounts can access them.

Why ETFs stayed available when international mutual funds paused

When SEBI imposed the overseas investment limit, existing ETF positions were not liquidated. The ETFs continued to trade on exchanges. Buyers and sellers transacted with each other — not with the AMC.

So the fund’s overseas investment limit was not consumed per transaction. This made international ETFs a practical alternative during the pause.

The NAV Premium Problem — What Every ETF Buyer Must Know

Here is the critical risk that most beginners overlook.

Because domestic AMCs cannot freely increase their overseas holdings beyond the SEBI/RBI cap, they cannot create new ETF units to meet demand. When investor interest in international markets spikes, the secondary market price of these ETFs rises — even if the underlying portfolio has not moved.

The result: you pay significantly more than the fund is actually worth.

Here is the actual premium data tracked in early March 2026:

| ETF | Premium to iNAV (Mar 2) | Premium to iNAV (Mar 9) |

|---|---|---|

| Mirae Asset Hang Seng TECH | 23% | 16% |

| Mirae Asset S&P 500 Top 50 | 21% | 17% |

| Mirae Asset NYSE FANG+ | 21% | 21% |

| Nippon Hang Seng BeES | 17% | 15% |

| Motilal Oswal Nasdaq 50 | 7% | 3% |

| Motilal Oswal Nasdaq 100 | 2% | 1% |

Paying a 21% premium means the underlying fund needs to deliver 21% just for you to break even. Premiums narrow when global momentum cools — meaning investors who bought at peak enthusiasm often sell at a loss even when the underlying market has risen.

The practical implication: Broad index ETFs — S&P 500, Nasdaq 100 — trade at far tighter premiums than thematic ones. If you invest through this route, check the premium before every purchase. Not just once.

Mutual Funds vs ETFs — Side by Side

| International Mutual Fund | International ETF | |

|---|---|---|

| How you buy | Through a fund platform or MFD | Through a demat account |

| Pricing | End-of-day NAV | Real-time market price |

| Minimum investment | ₹500 SIP in most cases | Price of 1 unit (varies) |

| SIP available? | Yes — straightforward | Possible but requires setup |

| Expense ratio | Slightly higher (FoF has dual layer) | Generally lower |

| NAV premium risk | Not applicable | High for thematic ETFs |

| Regulatory constraint | Subject to SEBI overseas cap | Less directly impacted |

| Tax (LTCG) | 12.5% | 12.5% |

| Ease of use | High — same as any SIP | Moderate — needs demat account |

LRS Direct Investing

The Liberalised Remittance Scheme (LRS) allows Indian residents to remit up to $250,000 per year overseas for investments.

You open an account with a foreign broker — platforms like Vested Finance, Interactive Brokers, INDmoney, or Paasa facilitate this for Indian residents.

Remit funds.

Invest directly in US-listed or globally-listed stocks and ETFs.

The key advantages:

- No SEBI overseas investment cap applies. You are not going through an Indian AMC.

- Access to the full universe of global ETFs — including products unavailable through the domestic route.

- LTCG taxed at 12.5% — same as Route 1.

The considerations:

- Currency conversion costs apply on every remittance.

- Tax filing complexity increases — foreign assets must be disclosed under Schedule FA in your ITR.

- Requires more active management than a SIP.

LRS is best suited for investors who are comfortable with a slightly higher operational overhead in exchange for broader access and no cap constraints.

What Is GIFT City?

This is the route most Indian investors have not heard of. And it is increasingly relevant.

GIFT City — Gujarat International Finance Tec-City — is India’s International Financial Services Centre (IFSC). It is a special economic zone that operates under a different regulatory framework from the rest of India.

Funds domiciled within GIFT City’s IFSC are treated as foreign funds for regulatory purposes. They are not subject to the $7 billion SEBI overseas investment cap that constrains domestic AMCs. This is the most structurally important distinction.

For an investor, this means: the pausing problem that affects feeder funds does not apply here.

Two Options Within GIFT City

| Investment Type | Minimum Ticket | Key Detail |

|---|---|---|

| Retail Funds | $5,000 | Fund houses operating outbound investment funds from GIFT City — open to Indian retail investors |

| PMS (Portfolio Management Services) | $1,50,000 | Targets larger investors operating from GIFT City. Some PMS structures are K-1 compliant — relevant for Indian-origin investors based in the US |

How Have GIFT City Funds Actually Performed?

GIFT City opened for outbound investing approximately four years ago. Five funds and several PMS structures are now operating. Here is the actual return data:

| Fund | Inception | Return Since Launch | ACWI (Benchmark) |

| DSP Global Equity Fund | Sept 2025 | −12.49% | +0.72% (6 months) |

| Philip International Pioneer PMS | — | −1.8% (6 months) | +0.72% (6 months) |

| Mirae Global | June 2024 | −0.57% | — |

| Philip International Fund | — | +7.70% since inception | +8.30% |

| Marcellus Global Compounders PMS | Dec 2021 | +18.60% since inception | +16.12% |

The performance picture is honest. Most funds are either behind benchmark or marginally ahead. DSP’s −12.49% since September 2025 reflects both a difficult global environment and the challenges of early-stage portfolio construction.

The one genuine alpha story is Marcellus Global Compounders PMS — +18.60% since December 2021 against the ACWI’s +16.12% over the same period. That is a meaningful outperformance over a four-year track record.

The context matters: the past six months have been broadly unkind to global equities. These are early-stage funds finding their footing. Performance will need to be tracked over a full market cycle before drawing firm conclusions.

A Note on Taxation Across All Routes

This is the area where most investors get the structure wrong.

Route 1 and Route 2 — Feeder Funds, ETFs, LRS Direct

Long-term capital gains are taxed at 12.5% — the same rate as domestic equity mutual funds held for more than one year above ₹1.25 lakh. However, international funds lost their indexation benefit after the Finance Act 2023. Gains are now added to income and taxed at slab rate if held for less than the qualifying period.

Tax Treatment in GIFT City

GIFT City funds are taxed differently from domestic international funds.

| Tax type | Holding period | Effective rate | Who pays |

|---|---|---|---|

Short-term capital gains Maximum marginal rate + surcharge + cess | Under 2 years | 42.7% | Fund |

Long-term capital gains 12.5% LTCG + surcharge + 4% cess | Over 2 years | 14.95% | Fund |

TCS on remittance Applies for LRS remittances above ₹10 lakh | At time of remittance | 20% Collected upfront | Investor |

Exit load Early withdrawal penalty | Withdrawal before 1 year | 1% | Investor |

ℹ️ Since the fund pays capital gains tax, resident Indian investors have zero additional tax liability at the time of redemption.

This is less favourable than Route 1 and Route 2, where LTCG is 12.5% regardless of holding period. Factor this into your net return calculations.

The broader point

How you combine domestic equity with international exposure — and when you book profits — now requires deliberate planning. This is not a decision to make in isolation. It is part of your overall portfolio tax strategy.

How Much of Your Portfolio Should Go International?

There is no universal answer. But there are useful frameworks.

Most global asset managers — including Vanguard and BlackRock — suggest allocating 15% to 30% of your equity portfolio to international markets.

Too little and the diversification benefit is negligible. Too much and you introduce currency volatility and complexity that may not suit your goals.

For a salaried professional with rupee-denominated goals — education, retirement, home — a 15% to 20% international allocation within the equity portion is a reasonable starting point.

The exact figure depends on four things:

- Your existing India exposure across funds

- Your investment horizon — longer horizons make international exposure more valuable

- Your rupee-denominated goals vs any future plans to live or study abroad

- Your comfort with currency volatility

These are not calculations to make alone. They are planning conversations.

Where International Investing Fits in Your Wealth Plan

International exposure is not a standalone strategy. It is a layer within a structured portfolio.

The R.S.W. Financial Independence Framework places international investing within the Core Investment layer — the part of your portfolio designed to grow wealth and fund long-term goals.

Your domestic equity allocation — through Flexi Cap, Large Cap, or Hybrid funds — forms the primary engine.

International exposure plays a supporting role. Diversification. Access to global growth. A partial currency hedge.

India-anchored. Globally diversified. That is what a structured portfolio looks like.

A Practical Starting Point

New to international investing? Here is a clean four-step approach.

1 Build your India equity base first. International investing before a solid domestic SIP is in place is the wrong sequence.

2 Decide on an allocation. Between 10% and 20% of your equity portfolio is the right range for most salaried professionals.

3 Choose your route. Start with Route 1 — feeder funds or index ETFs (S&P 500, Nasdaq 100). These carry the lowest premiums, the simplest SIP process, and the most favourable tax treatment.

Check the NAV premium before every ETF purchase. Avoid thematic ETFs until you understand the premium risk.

4 Get the tax planning right. Your advisor must factor your international allocation into your overall portfolio tax plan. This is not a separate decision. It is part of the same structure.

GIFT City and LRS Direct are routes to layer in as your portfolio and understanding grow — not where you begin.

Thinking About This Further?

The concept of international investing is simple. The execution — right route, right instrument, right allocation, right tax structure — benefits from a structured conversation.

What fits your portfolio depends on what you already hold, what your goals are, and how you want to manage the tax outcome year on year.

If you would like to understand where international exposure fits in your specific situation, we are happy to walk through it with you.

Book your free one-hour wealth planning call →

No commitment. No product pitch. Just a structured conversation about your portfolio and where international investing fits in it.

Nitin R Wali is a Chartered Wealth Manager (CWM®), AMFI Registered Mutual Fund Distributor (ARN–244802), and APMI Registered PMS Distributor (APRN07002) based in Pune, India. This article is for educational purposes only and does not constitute personalised financial advice. Tax laws are subject to change — consult a qualified advisor before making investment decisions.

Book your free one-hour wealth planning call →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years