1. What is portfolio rebalancing?

Portfolio rebalancing is the process of restoring your investments to their original target allocation — by selling what has grown overweight and buying what has fallen underweight — so the risk you carry stays aligned with the risk you chose.

1a. Why it matters

When you first invested, you chose a mix deliberately.

Perhaps 60% equity, 30% debt, 10% gold — reflecting your income, your goals, and how much of a fall you could absorb without panic.

Markets do not respect that decision.

A strong equity rally quietly pushes your 60% to 72%, then higher.

For a salaried investor managing a home loan, a child’s education, and a retirement corpus simultaneously, that unnoticed drift is a structural threat to every goal you are working toward.

1b. How it works

Rebalancing means selling units of your overweight asset — typically equity after a rally — and deploying the proceeds into underweight assets.

Alternatively, redirect fresh SIP contributions toward the underweight category, avoiding a sale and reducing tax impact.

Either way: restore the original balance, the risk level you chose, and the alignment between your portfolio and your life.

2. What is portfolio drift?

Portfolio drift is what happens between your decisions.

You chose your allocation deliberately — 60% equity, 30% debt, 10% gold.

You set up your SIPs and moved on. And while you were not watching, the market quietly restructured your portfolio for you.

There is no notification. No warning.

The corpus grows, the numbers look encouraging, and underneath that surface your equity allocation has silently moved from 60% to 70% to higher — carrying a risk level you never agreed to.

2a. How drift happens

Drift is a mathematical inevitability. Equity outperforms debt over sustained periods — which is why you invest in it.

But that same outperformance makes equity an ever-larger share of your wealth if left unmanaged.

| Asset class | Opening value | Returns | Closing value | New allocation |

|---|---|---|---|---|

| Equity | ₹6,00,000 | 25% | ₹7,50,000 | 68.5% |

| Debt | ₹3,00,000 | 7% | ₹3,21,000 | 29.3% |

| Gold | ₹1,00,000 | 10% | ₹1,10,000 | 10.0% |

| Total | ₹10,00,000 | ₹10,96,000 | 100% |

2b. Why it matters

A 30% correction on a drifted 70% equity portfolio produces a drawdown of ₹2,30,000.

The same correction on a disciplined 60% portfolio produces ₹1,80,000. That ₹50,000 difference is a goal delayed or a financial decision made under pressure.

Drift does not just increase volatility. It increases the likelihood that a market correction forces a life decision you were not prepared to make.

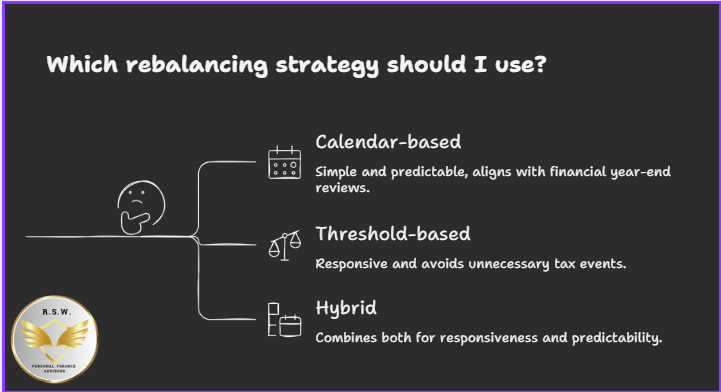

3. Rebalancing strategies : Which one is right for you ?

3a. Calendar-based rebalancing

Review and rebalance at fixed intervals — annually, semi-annually, or quarterly — regardless of drift. Annual rebalancing suits most salaried investors: it aligns with your financial year-end review, tax planning, and goal reviews.

Simple and predictable.

The limitation: significant drift between reviews goes uncorrected for months.

3b. Threshold-based rebalancing (band rebalancing)

Rebalance only when an asset class drifts beyond ±5% from its target.

More responsive than calendar rebalancing and avoids unnecessary tax events in stable markets.

Requires periodic monitoring even when action is infrequent.

3c. Hybrid rebalancing

Combine both: review annually, but act immediately if drift crosses the threshold. Review every April.

Check quarterly. Act only if drift has crossed 5%. Otherwise, wait for April.

3d. Which strategy suits Indian investors best

For most salaried investors, the hybrid approach at ±5% with an annual review is the most sensible starting point — disciplined enough to prevent dangerous drift, tax-efficient enough to avoid unnecessary redemptions.

| Strategy | Best for | Review frequency | Acts when | Tax impact |

|---|---|---|---|---|

| Calendar | Hands-off investors | Annually / semi-annually | Fixed date, regardless of drift | Moderate |

| Threshold (±5% band) | Active monitors | Ongoing monitoring | Drift crosses 5% | Lower |

| Hybrid (recommended) | Most salaried investors | Quarterly check, annual action | Drift crosses 5% or April review | Lowest |

4. Rebalancing : Across Differenete Asset Classes

4a. Mutual Funds

For most Indian salaried investors, the portfolio is built almost entirely through mutual funds.

Mutual fund rebalancing means correcting drift by redeeming overweight fund units, switching between funds within the same folio, or redirecting fresh SIP contributions toward underweight categories.

A worked example — Arjun’s portfolio, Pune

Arjun is 38, works in IT, and started his mutual fund journey in April 2022 with ₹10 lakhs:

| Asset class | Fund | Target allocation | Amount invested |

| Equity | Nifty 50 Index Fund | 60% | ₹6,00,000 |

| Debt | Short Duration Debt Fund | 30% | ₹3,00,000 |

| Gold | Gold ETF / Fund of Fund | 10% | ₹1,00,000 |

By April 2024, his portfolio has grown to ₹14 lakhs — but not evenly:

| Asset class | Current value | Current allocation | Target allocation | Drift |

|---|---|---|---|---|

| Equity | ₹9,80,000 | 70% | 60% | +10% overweight |

| Debt | ₹3,36,000 | 24% | 30% | -6% underweight |

| Gold | ₹84,000 | 6% | 10% | -4% underweight |

| Total | ₹14,00,000 | 100% | 100% |

To restore his 60-30-10 allocation:

| Asset class | Target value | Current value | Action required |

|---|---|---|---|

| Equity | ₹8,40,000 | ₹9,80,000 | Redeem ₹1,40,000 |

| Debt | ₹4,20,000 | ₹3,36,000 | Invest ₹84,000 |

| Gold | ₹1,40,000 | ₹84,000 | Invest ₹56,000 |

Arjun has done the right thing. But what if he had not? Here is what his portfolio would be silently carrying:

| Asset class | Current value | Allocation | Target | Drift | If left uncorrected |

|---|---|---|---|---|---|

| Equity | ₹9,80,000 | 70% | 60% | +10% | A 30% correction wipes out ₹2,94,000 — not ₹1,80,000 as planned |

| Debt | ₹3,36,000 | 24% | 30% | -6% | Stability cushion shrinks. Less capital to redeploy during corrections |

| Gold | ₹84,000 | 6% | 10% | -4% | Inflation hedge weakens. Portfolio more vulnerable to macro shocks |

| Total | ₹14,00,000 | 100% | 100% | Risk profile has silently shifted from moderate to aggressive |

Portfolio Rebalancing Calculator

Enter your current and target allocation to find out exactly what to buy or sell.

The smarter alternative — SIP redirection

If Arjun has active monthly SIPs, he can pause his equity SIP and redirect contributions to debt and gold until allocation normalises.

No redemption. No tax event. Same outcome over 3–4 months.

This is the most tax-efficient rebalancing method available to Indian mutual fund investors — and the most underused.

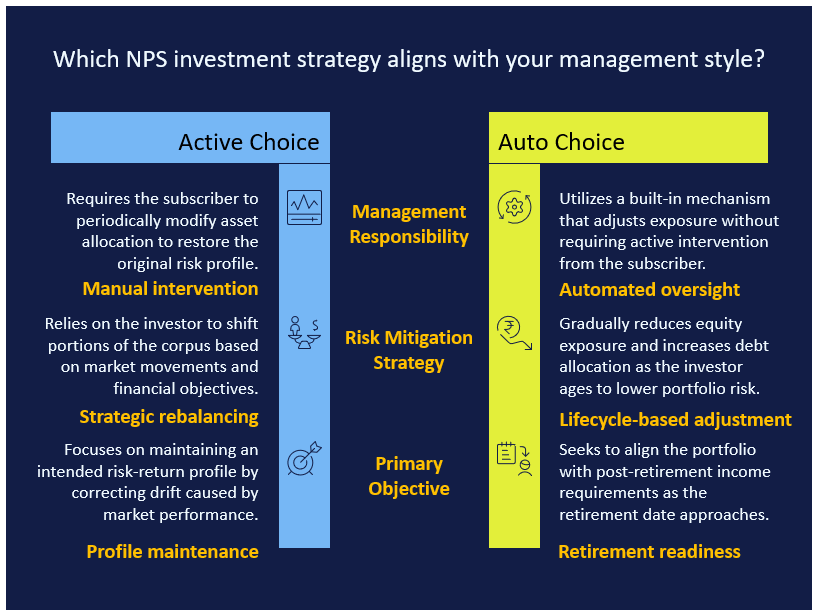

4b. National Pension Scheme [NPS]

Portfolio rebalancing is equally relevant within the National Pension System (NPS), though it works somewhat differently from traditional investment portfolios. The objective remains the same: maintaining the desired asset allocation and risk profile over time.

Active Choice in NPS can allocates investments across Equity (E), Corporate Debt (C), Government Securities (G), and Alternative Investments (A). As markets move, the actual allocation may drift away from the intended allocation. For example, an investor targeting 75% equity may find the equity allocation rising to 82% after a prolonged bull market. In such situations, rebalancing helps restore the original risk profile.

NPS facilitates this process by allowing subscribers to modify their asset allocation periodically. Rebalancing may involve shifting a portion of the accumulated corpus from equity to debt or vice versa, depending on market movements and the investor’s financial objectives.

Auto Choice experience a form of automatic rebalancing. The NPS lifecycle funds gradually reduce equity exposure and increase debt allocation as the investor ages. This built-in mechanism seeks to lower portfolio risk as retirement approaches without requiring active intervention from the subscriber.

Rebalancing becomes particularly important during the years leading up to retirement. A significant market correction just before retirement can have a disproportionate impact on the accumulated corpus.

Gradually reducing equity exposure and aligning the portfolio with post-retirement income requirements can help manage this risk.

However, NPS rebalancing should not be driven by short-term market forecasts or attempts to time the market. Instead, it should be guided by changes in asset allocation, risk tolerance, time horizon, and retirement goals. The purpose is not to maximize returns but to ensure that the portfolio continues to reflect the investor’s intended risk-return profile throughout the accumulation journey.

A detailed discussion on NPS portfolio rebalancing, including Active Choice, Auto Choice, lifecycle funds, and pre-retirement strategies, is covered separately in our comprehensive guide on NPS portfolio management.

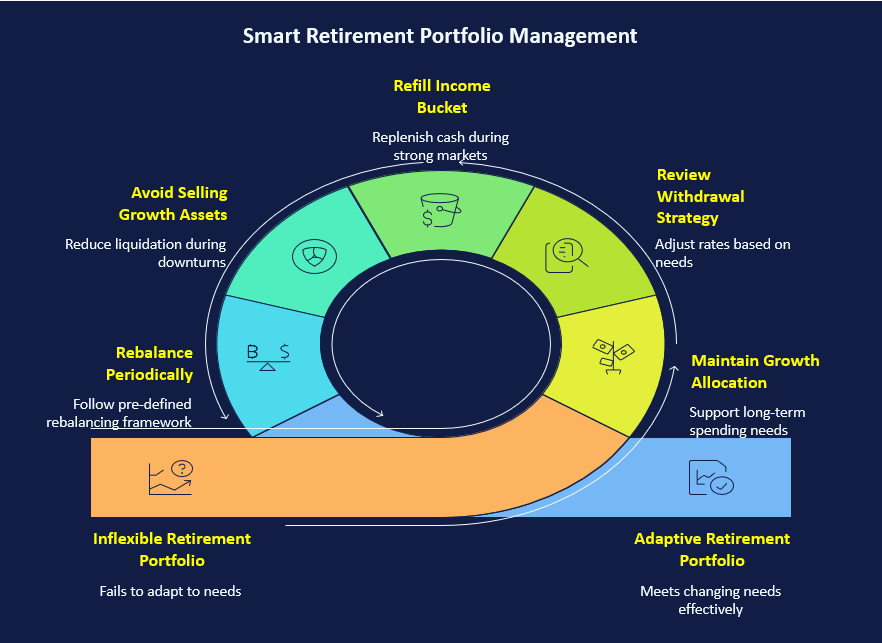

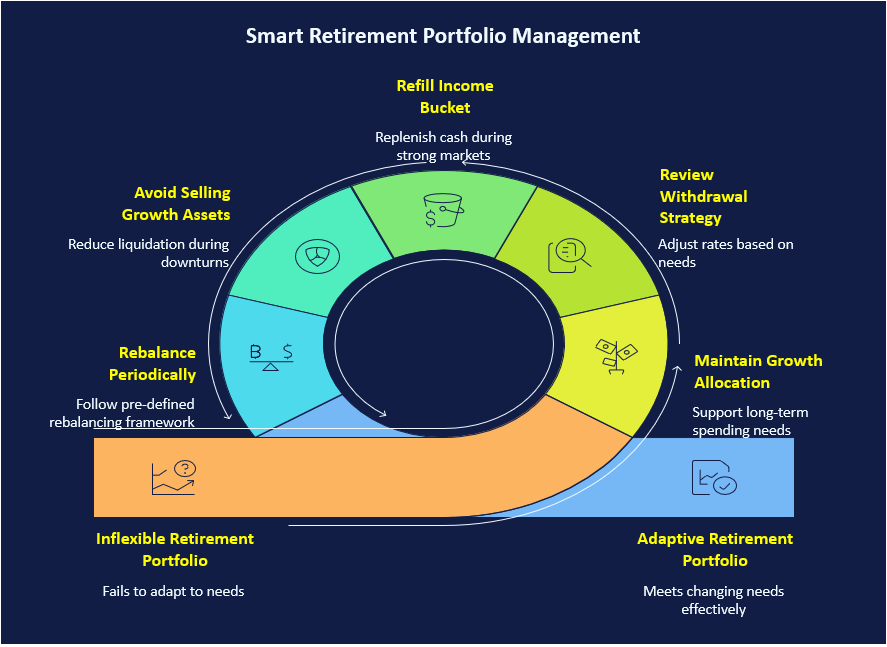

4c. Portfolio Rebalancing at Retirement

Portfolio rebalancing assumes a different significance as investors approach retirement. During the accumulation years, a market decline can often be viewed as a temporary setback because future savings and a long investment horizon provide opportunities for recovery. However, the years immediately preceding retirement represent a vulnerable phase. A sharp market correction just before retirement can permanently alter the lifestyle that the accumulated corpus is expected to support.

This is often referred to as sequence-of-return risk—the risk of experiencing poor market returns just as the portfolio transitions from wealth creation to wealth distribution. Two investors earning identical long-term average returns can experience very different retirement outcomes depending on the order in which those returns occur.

As retirement approaches, investors may consider the following principles:

- Protect near-term retirement expenses: The portion of the portfolio expected to fund the first 2–3 years of retirement may gradually be shifted towards relatively stable assets.

- Retain growth for long-term needs: Retirement can span 25–30 years. Maintaining an allocation to growth assets such as equities can help combat inflation.

- Reduce abrupt allocation changes: Instead of moving from 70% equity to 20% equity overnight, a phased transition over the last few years before retirement may be more appropriate.

- Review withdrawal needs: The planned income requirement after retirement should influence the rebalancing strategy.

- Avoid emotional decisions: Large market movements close to retirement often trigger fear or greed. Rebalancing should be guided by a pre-defined plan rather than short-term market sentiment.

The objective is not to eliminate risk altogether, but to ensure that the portfolio remains aligned with both the immediate income needs and the long-term realities of retirement. In many ways, the years around retirement represent the most critical period for disciplined rebalancing, as decisions taken during this transition can influence financial security throughout retirement.

4d. Portfolio Rebalancing After Retirement

Portfolio rebalancing remains equally important after retirement. Unlike the accumulation phase, retirees are withdrawing from their portfolios while managing inflation, market volatility and longevity risk. Becoming overly conservative may protect against short-term fluctuations, but it can also reduce the portfolio’s ability to support a retirement that may last several decades.

Some practical considerations include:

- Retain some growth assets to help combat inflation over the long term.

- Review withdrawal needs periodically and align the portfolio accordingly.

- Maintain a reserve for near-term expenses to avoid selling growth assets during market downturns.

- Rebalance based on a pre-defined plan rather than reacting to market movements.

The objective of rebalancing after retirement is to strike a balance between preserving capital for today’s needs and maintaining sufficient growth for tomorrow’s expenses.

5. Tax implications of rebalancing in India

Every redemption for rebalancing is a potential tax event. Tax treatment depends on fund type, holding period, and purchase date.

The table below reflects Union Budget 2024 changes, effective July 23, 2024, per the official CBDT FAQ.

| Fund type | Short-term (STCG) | Long-term (LTCG) |

|---|---|---|

| Equity mutual funds | 20% (under 12 months) | 12.5% on gains above ₹1.25 lakh |

| Debt mutual funds (purchased after April 1, 2023) | Slab rate | Slab rate |

| Balanced Advantage Funds (65%+ equity) | 20% (under 12 months) | 12.5% on gains above ₹1.25 lakh [ Over 12 Months ] |

| Gold Fund of Fund | Slab rate (under 24 months) | 12.5% without indexation [ Over 24 months] |

On Arjun’s ₹1.40 lakh redemption, the difference between units held 11 months versus 13 months is approximately ₹10,500 in avoidable tax. A few weeks of patience saves it entirely.

5a. The debt fund rule most investors miss

From April 1, 2023, all capital gains from debt mutual funds are taxed at the investor’s income slab rate — regardless of holding period.

For a salaried professional in the 30% bracket, this is a threefold increase in tax cost compared to the pre-2023 regime.

Use SIP redirection into debt rather than lump sum switches wherever possible.

5b. The ₹1.25 lakh LTCG exemption — use it deliberately

The first ₹1.25 lakh of LTCG across equity shares and equity-oriented funds is exempt from tax each financial year.

A disciplined rebalancing practice can harvest up to this limit annually — reducing equity overweight, restoring allocation, and paying zero tax on the redemption.

5c. Tax-first rebalancing sequence

1. Can SIP redirection correct the drift? If yes — no tax event.

2. Are units older than 12 months? If not — wait where possible.

3. How much of the ₹1.25 lakh annual exemption remains? Redeem up to that limit first.

4. Is the date close to March 31? Split across two financial years to double the exemption.

6. When and how often should you rebalance? Your RSW stage decides

Age-based rules — ‘hold your age in debt’ — are a starting point.

But where you are in your financial journey matters more than your birthday.

The RSW Financial Independence Framework organises that journey into five stages.

Your rebalancing approach should be anchored to your current stage.

| RSW stage | Primary focus | Rebalancing priority | Rebalancing trigger |

| Stage 1: Cash flow & money management | Surplus creation, Debt rationalisation | Low | Annual review only |

| Stage 2: Emergency fund & risk protection | Protection before growth | Low | Annual review only |

| Stage 3: Goal-based planning | 1. Home 2. Education 3. Retirement corpus | High — Goals have deadlines | Hybrid: ±5% threshold + annual |

| Stage 4: Wealth creation & capital growth | 1. Accelerating returns, 2. Tax efficiency | High | Hybrid: ±5% + quarterly check |

| Stage 5: Estate planning & legacy | Preservation and succession | Critical | Threshold-based: ±3% band |

A 42-year-old in Stage 2 — carrying inadequate insurance and no emergency fund — should not be running a 70% equity portfolio regardless of age.

Rebalancing is a Stage 4 discipline. It works best when Stages 1, 2, and 3 are already in place.

6a. Goal proximity overrides everything

As a goal approaches within 3 years, begin de-risking that specific corpus — irrespective of where the market is.

| Goal horizon | Suggested equity allocation [For that goal’s corpus] |

|---|---|

| More than 7 years away | 70–80% equity |

| 4–7 years away | 50–60% equity |

| 2–3 years away | 20–30% equity |

| Under 2 years away | 0–10% equity |

Rebalancing does not exist in isolation.

It is one of four disciplines in Stage 4 of the RSW Financial Independence Framework — alongside core and tactical asset allocation, blue-chip stock ownership, and tax efficiency optimisation.

Understand where you stand in the RSW Financial Independence Framework →

7. Do Balanced Advantage Funds rebalance for you?

A Balanced Advantage Fund — officially classified by SEBI as a Dynamic Asset Allocation Fund — automatically shifts allocation between equity and debt based on market valuations.

Internal reallocation happens at the fund manager level. You do not monitor drift, calculate sell amounts, or trigger a tax event.

| Feature | Manual rebalancing | Balanced Advantage Fund |

|---|---|---|

| Who monitors drift | You | Fund manager |

| Rebalancing trigger | Your review | Model-driven, continuous |

| Tax on rebalancing | Capital gains on redemption | No tax — internal reallocation |

| Effort required | Moderate — periodic action needed | None — fully automated |

| Control over allocation | Full | Limited — fund follows its own model |

| Expense ratio | Lower — index funds + your time | Higher — active management cost |

The fundamental trade-off: you gain convenience and tax efficiency on internal rebalancing, but you cede allocation control to a model that does not know your goals.

Within the RSW Framework, BAFs work best as a core holding in Stage 3 for medium-horizon goals, or as a satellite allocation in Stage 4 alongside a manually managed portfolio.

They are not a replacement for a financial plan. They are a tool within one.

8. 5 rebalancing mistakes Indian investors make

1: Rebalancing on emotion, not rules

Selling equity after a correction because it ‘feels risky’ is panic-selling with a respectable name.

Rebalancing works only when rules-driven. Define your threshold before the market moves — not after.

2: Ignoring tax before redeeming

Selling equity units held under one year generates STCG at 20% — often avoidable by waiting a few weeks or redirecting SIP inflows.

Always check the purchase date of each unit lot before acting. Older units first.

3: Rebalancing the whole portfolio when only one goal has drifted

Your home corpus, education corpus, and retirement corpus have different horizons and targets.

Track and rebalance each goal corpus independently.

4: Over-rebalancing in volatile markets

Frequent rebalancing generates tax events and costs without improving outcomes.

The return difference between annual and quarterly rebalancing is marginal.

The cost difference is not. Volatility is not a trigger. Drift is.

5: Assuming a Balanced Advantage Fund means your portfolio is rebalanced

A BAF rebalances internally.

But if your portfolio also includes EPF, PPF, NPS, gold, and direct equity — the BAF is one component, not the whole picture. Review your complete net worth allocation annually.

9. Frequently asked questions about portfolio rebalancing

Rebalancing is the process of restoring your portfolio to its original target allocation — by selling assets that have grown overweight and buying those that have fallen underweight. It is not about predicting markets. It is about enforcing the risk level you originally chose.

In mutual funds, rebalancing means correcting drift by redeeming overweight fund units, switching between categories, or redirecting SIP contributions toward underweight asset classes without triggering a redemption.

Amount to sell or buy = Current value of asset − (Target % × Total portfolio value)

If your equity target is 60% on a ₹14 lakh portfolio, target equity value is ₹8.40 lakhs. If equity is currently ₹9.80 lakhs, redeem ₹1.40 lakhs and deploy into underweight assets. Use the rebalancing calculator on this page for your exact numbers.

A ±5% drift from target allocation, reviewed annually with a quarterly check, works well for most salaried investors — balancing discipline with tax efficiency.

Yes, whenever rebalancing involves redemption.

Equity fund units held under one year attract STCG at 20%.

Units held over one year attract LTCG at 12.5% on gains above ₹1.25 lakh. Debt funds sold after April 2023 are taxed at your slab rate. Use SIP redirection where possible to avoid a tax event.

Not necessarily — and that is not its purpose. In a bull market, rebalancing modestly reduces returns by trimming the best-performing asset.

What it reliably does is reduce drawdown risk and ensure your portfolio reflects your strategy, not the market’s momentum.

Switching is a quality decision within an asset class

.

Rebalancing is an allocation decision — correcting how much of your total portfolio sits in each asset class.

Both trigger tax events.

Only rebalancing restores your intended risk profile.

Your portfolio will drift. The market guarantees it. What you choose to do about it — and when — is the only variable within your control.

Begin your rebalancing review for you Portfolio [ Book a Call ] →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”