Most conversations about ETF investing in India start with the same premise:

ETFs are low-cost, transparent, and passively managed. Therefore, you should use them.

That is not wrong. But it is incomplete — in a way that causes real portfolio damage.

What Exactly Is an ETF?

An Exchange-Traded Fund — ETF — is a basket of securities that trades on a stock exchange, just like a share.

When you buy one unit of a Nifty 50 ETF, you are not buying one company. You are buying a small slice of all 50 companies in the index — in one transaction, at one price, with one expense ratio.

Three things define how it works:

Tracks an index — it does not pick stocks, it mirrors one.

Trades on an exchange — bought and sold during market hours at a live price, not at end-of-day NAV like a mutual fund.

Requires a demat account — the most important structural difference from a regular mutual fund, with significant practical implications we will return to.

The question is not whether ETFs are good instruments.

The question is:

- Good for what,

- At which stage of your wealth journey,

- For which type of investor?

These are not the same question. And the answer to each one is different.

At RSW Personal Finance Advisors, every investment recommendation is evaluated through the lens of the RSW Financial Independence Framework — a five-stage structure built specifically for salaried professionals in India.

The Framework’s logic is sequential: protection before growth, goals before allocation, structure before performance.

When you evaluate ETFs through this lens, a clear and perhaps surprising picture emerges. Some ETFs belong firmly in the core of a long-term portfolio.

Others belong only in a tactical, time-limited role. And some have no place in a salaried investor’s wealth plan at all — regardless of how enthusiastically they are marketed.

Why Instrument Suitability Is Stage-Dependent

Here is the foundational idea that most ETF articles miss entirely.

The same instrument can be the right choice at one stage of your wealth journey and the wrong choice at another. Not because the instrument changed — but because your financial situation, your deployment mode, your goal timeline, and your behavioural needs changed.

The RSW Financial Independence Framework maps wealth building across five stages:

- Stage 1 — Managing Money: Cash flow control, debt rationalization, surplus creation

- Stage 2 — Build Safety Net: Emergency fund, term insurance, health insurance

- Stage 3 — Fund Core Life Goals: Home, children’s education, retirement

- Stage 4 — Accelerate Wealth: Capital growth beyond core goals, core and tactical allocation

- Stage 5 — Build Legacy: Estate planning, succession, generational continuity

Each stage has a different relationship with risk, liquidity, and instrument complexity. And ETF suitability shifts across every single one.

The ETF Universe in India: Eight Categories, Eight Different Portfolio Roles

India’s ETF landscape has expanded significantly. But expansion has also created confusion — because “ETF” now covers instruments with fundamentally different risk profiles, purposes, and portfolio roles.

| ETF Category | Examples | What Does This Mean? |

|---|---|---|

| Broad-Market Equity | Nifty 50, Sensex, Nifty 100, Nifty 500 | Tracks an index that covers a large number of companies across multiple sectors. When you buy one unit, you effectively own a small slice of India’s top companies — across industries, not just one. |

| Market Capitalisation | Nifty Midcap 150, Nifty Smallcap 250 | Tracks companies grouped by their size — mid-sized or smaller companies. These are businesses beyond the well-known large caps, with higher growth potential but also higher price swings. |

| Sectoral | Nifty Bank, Nifty IT, Nifty Pharma, Nifty Auto, Nifty Infrastructure | Tracks only the companies within one specific industry. If that industry does well, the ETF rises. If that industry faces a downturn, the entire ETF falls — there is no cushion from other sectors. |

| Thematic | PSU Revival, Defence, Manufacturing, Consumption, ESG | Built around a specific investment story or trend — for example, India’s defence spending or the rise of domestic manufacturing. The ETF rises or falls based on how that story plays out in the market. |

| Smart Beta / Factor | Momentum, Quality, Low Volatility, Value | Uses a set of rules to select stocks — not purely by market size, but by a specific characteristic like recent price momentum, earnings quality, or lower price volatility. A hybrid between passive and active. |

| Commodity | Gold ETF, Silver ETF | Tracks the price of a physical commodity. A Gold ETF, for instance, moves with the price of gold — giving you the benefit of gold ownership without holding it physically. |

| Debt | Bharat Bond ETF, G-Sec ETFs, PSU Bond ETFs | Tracks a basket of bonds — essentially loans given to the government or public sector companies. These pay interest and return capital at maturity. Lower risk than equity, but also lower return potential. |

| International | Nasdaq 100, S&P 500, Hang Seng, MSCI World | Tracks stock indices of foreign markets. Allows an Indian investor to participate in the growth of US technology companies, global multinationals, or emerging market economies — from a single Indian rupee investment. |

Eight categories. Eight different risk, return, liquidity, and behavioural profiles. Treating them as a single category called “ETFs” and assigning them a uniform portfolio role is one of the most common structural errors in retail portfolio construction today.

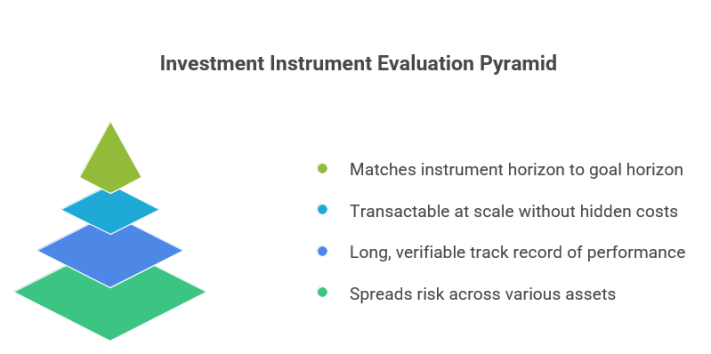

What Actually Makes an ETF “Core” — The Four-Point Test

In portfolio construction, “core” has a precise meaning. A core investment:

- Anchors long-term wealth creation across market cycles

- Operates without requiring active management decisions

- Reduces portfolio complexity rather than adding to it

- Keeps working when you are not watching it

Applying the Four-Point Test

1: Broad diversification — does it spread risk or concentrate it?

A core ETF must hold a sufficiently large and diversified basket of securities that no single sector, policy event, or corporate development can materially damage the portfolio. The Nifty 50 holds India’s 50 largest companies across 13+ sectors. A Nifty Bank ETF holds 12 banks. The first is a diversified equity position. The second is a concentrated sector bet.

If one adverse event — a credit cycle turn, a regulatory change, a global technology downturn — can inflict significant damage to the ETF, it does not belong in the core.

2: Structural stability — does the index have a long, verifiable track record?

Core instruments are held for 15–25 years. An ETF tracking a newly constructed thematic index — assembled around a trend that emerged three years ago — has no basis for long-term reliability. The methodology may be reconstituted. The theme may structurally fade. The index construction rules may change.

Nifty 50 has a 25+ year history. The Nifty India Defence Index was launched in 2021. These are not comparable as core anchors. Recency of the index is a disqualifying factor for core consideration.

Tracking error and bid-ask spread are the invisible costs of ETF investing. A core ETF must have high trading volumes and tight spreads. For smaller, less liquid ETFs, placing a ₹5–10 lakh order meaningfully moves the market price. The execution cost eats directly into the cost advantage that ETFs are supposed to deliver.

Illiquid ETFs should not be in a core portfolio. In some cases, they should not be in a retail portfolio at all.

4: Goal-timeline alignment — does the instrument match the horizon of the goal it funds?

A Nifty 50 ETF placed in a portfolio earmarked for a goal three years away is a structural mismatch — regardless of the instrument’s quality. Core suitability is always evaluated in the context of the specific goal it serves, not in the abstract.

ETF Role Mapped to the RSW Five-Stage Framework

This is the table that most ETF discussions in India do not provide — a clear mapping of which ETFs are appropriate at which stage of a salaried investor’s wealth journey.

| RSW Stage | Financial Priority | ETF Role | Appropriate ETF Types |

|---|---|---|---|

| Stage 1: Managing Money | Surplus creation, debt control | None | — |

| Stage 2: Build Safety Net | Emergency fund, insurance | None | — |

| Stage 3A: Education Goal | 10–15 year horizon | Core equity layer, progressively de-risked | Nifty 50 ETF, Nifty 100 ETF (or index fund equivalent) |

| Stage 3B: Retirement | 20–30 year horizon | Core equity + core debt layer | Nifty 50 / Nifty Next 50 ETF + Bharat Bond ETF |

| Stage 4: Accelerate Wealth | Capital growth | Core passive ETF + tactical satellite layer | Broad ETF as core; midcap, sectoral, international ETF as tactical |

| Stage 5: Build Legacy | Estate, succession | Simplification | Consolidate into broad ETFs for ease of inheritance |

Three observations that matter:

Stages 1 and 2 are ETF-free zones. The foundation — cash flow, emergency fund, insurance — must be in place before any growth instrument is introduced.

Stage 3 is where ETFs earn their most important role. Education and retirement have long enough horizons for broad-market ETFs to deliver their core advantage: low cost, broad diversification, and no active management risk. This is where the Four-Point Core Test matters most.

Stage 4 is where Core and Tactical architecture takes shape. A broad-market ETF anchors the core; tactical positions — midcap, sectoral, international — are sized around it with a clear thesis and exit discipline.

For a detailed treatment of this architecture, see the Core and Tactical Allocation guide for Indian investors.

Core ETF :

| ETF | What It Invests In | Why It Qualifies as Core |

|---|---|---|

| Nifty 50 ETF | India’s top 50 large-cap companies across 13+ sectors | Broadest diversification, 25+ year index history, – highest liquidity, – lowest expense ratios (0.05–0.10%) |

| Nifty Next 50 ETF | The next 50 large-cap companies ranked just outside the Nifty 50 | Adds diversification beyond the top 50, strong long-term return history, adequate liquidity |

| Nifty 100 ETF | Top 100 large-cap companies — combines Nifty 50 and Nifty Next 50 in one instrument | Single instrument, broad large-cap coverage, simplifies portfolio management |

| Nifty 500 ETF / Index Fund | Top 500 companies across large, mid, and small cap | Widest market coverage in a single instrument, no need to manage multiple ETFs |

| Gold ETF | Physical gold prices | Non-correlated with equity — acts as a portfolio stabiliser and inflation hedge |

| Bharat Bond ETF | AAA-rated PSU bonds with defined maturities | Transparent, low cost, tax-efficient for investors in higher tax brackets on 3+ year horizon |

For Tactical Layer — Not the Core

| ETF | What It Invests In | Why It Is Tactical — Not Core | When It Makes Sense |

|---|---|---|---|

| Nifty Midcap 150 / Smallcap 250 ETF | Mid-sized and smaller companies beyond the top 100 | Drawdowns of 40–60% in bear markets are structural, not exceptions. Too volatile to anchor a core portfolio | As a 10–15% position alongside — not instead of — a broad-market core ETF |

| Sectoral ETFs — Banking, IT, Pharma, Infrastructure, Auto | All companies within one specific industry | Sectors cycle. Concentration in one sector removes the protection that diversification provides | Only when you have a specific, time-bound view on a sector — and the discipline to exit when that thesis plays out or fails |

| Nifty Momentum 30 / Smart Beta ETFs | Stocks selected by a specific factor — momentum, quality, low volatility, value | Factor cycles are real and prolonged. Momentum underperforms sharply in market reversals. Not a set-and-forget instrument | For investors who actively track their portfolio and understand the factor they are expressing |

| International ETFs — Nasdaq 100, S&P 500 | Stocks listed on foreign exchanges | Regulatory constraints, currency risk, and higher costs than domestic ETFs. Overweighting introduces risks most salaried investors have not accounted for | A 10–15% geographic diversifier for Stage 4 investors with a clear understanding of currency and regulatory risk |

ETFs That Have No Place in a Long-Term Wealth Plan

| ETF | The Appeal | Why It Does Not Belong |

|---|---|---|

| Thematic ETFs — Defence, EV, Green Energy, Digital Transformation | Compelling sector stories with strong near-term narratives | Most indices constructed post-2020 — no long-term track record. Concentrated holdings, lower liquidity, and performance entirely dependent on the narrative staying intact. When the story fades, there is no clear signal of recovery |

| Silver ETF | AUM grew 126% in 2024–25 — rising investor interest signals opportunity | More volatile than gold, less predictable price cycle, significant industrial demand linkage. As a 2–3% tactical position — possibly. As a structural holding in a wealth plan — misaligned with any core allocation purpose |

| Inverse and Leveraged ETFs | Appear to offer downside protection or amplified returns | Built for institutional hedging and short-term trading only. Daily rebalancing causes return decay over time — the longer you hold, the further they drift from their stated objective. No role in a long-term wealth plan |

Index Fund vs ETF :

The parallel instrument to a Nifty 50 ETF is a direct plan Nifty 50 index fund — same market exposure, marginally different cost structure, and a fundamentally different execution experience.

Here is how they compare:

| Factor | Direct Plan Index Fund | Nifty 50 ETF |

|---|---|---|

| Expense Ratio | 0.20–0.50% | 0.05–0.35% |

| Total Cost | Expense ratio only | Expense ratio + brokerage + STT + bid-ask spread |

| SIP Auto-debit | Native and seamless | Broker-dependent; manual funding required |

| Demat Account | Not required | Mandatory |

| Fractional Units | Yes | No — whole units only |

| Intraday Pricing | No | Yes |

| Best Suited For | Monthly SIP investors, all corpus sizes | Lump sum deployment, ₹25 lakh+ corpus |

The Accumulation Phase Problem — The Most Practical Issue Nobody Addresses

Here is the structural reality that most ETF discussions in India skip.

The salaried investor’s primary deployment mechanism is the monthly SIP. A fixed amount, auto-debited from the salary account, invested without manual intervention.

This is not just a preference — it is the behavioural architecture that makes long-term wealth creation work for working professionals.

Automation removes the decision from the equation. Removing the decision removes the emotion. Removing the emotion allows compounding to work undisturbed.

ETFs, by design, do not support native SIP auto-debit.

When you start a mutual fund SIP, the AMC debits your bank account directly and allots fractional units at that day’s closing NAV.

No demat account, manual funding, lot-size constraint.

Set and forget.

When you invest in an ETF systematically, the mechanism is fundamentally different.

The ETF SIP is a broker-platform feature — not a fund house facility. Your trading ledger must carry cleared funds before the investment date. ETFs trade in whole units, so ₹5,000 invested in an ETF priced at ₹300 buys 16 units (₹4,800), leaving ₹200 uninvested in your trading account indefinitely.

There is no fractional unit allocation. Not every broker offers automated ETF SIP, and those that do vary significantly in reliability.

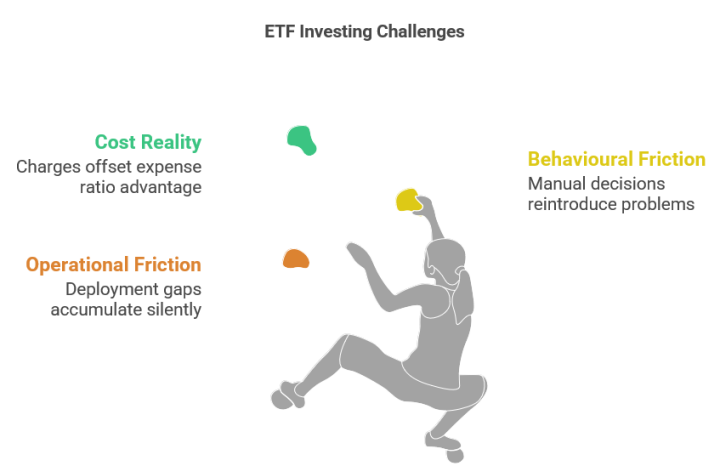

In practice, this means three real friction points:

Operational friction:

ETF investing requires an active demat and trading account relationship — funded correctly, on time, every month. When this slips — a holiday, a bank processing delay, a forgotten top-up — deployment gaps accumulate silently.

Behavioural friction:

Monthly active involvement in ETF investment decisions reintroduces the very decision-making opportunities that automation was designed to eliminate. When markets are down, the manual nature of ETF SIP gives investors a choice — which is precisely the problem.

Cost reality:

The ETF expense ratio advantage (0.05–0.35% vs. 0.20–0.50% for direct plan index funds) is real but smaller than it appears in isolation. The total cost of ETF investing includes brokerage charges, Securities Transaction Tax, and bid-ask spread on every transaction. For monthly SIP amounts of ₹5,000–₹25,000, these transaction costs partially or fully offset the expense ratio advantage.

The honest advisory position: if your primary mode is monthly SIP and you do not have an active, well-managed demat relationship, a direct plan Nifty 50 index fund will serve your core equity allocation better than a Nifty 50 ETF in most practical scenarios.

Not because the ETF is inferior — but because the execution environment does not support it properly.

When the ETF Becomes the Right Core Vehicle — The Phase Shift

The ETF calculus changes meaningfully once you cross into what we call the consolidation phase — typically Stage 4 of the RSW Framework, when core life goals are funded and lump sum deployment becomes the primary mode alongside ongoing SIPs.

At a corpus of ₹25 lakh and above in a specific goal’s portfolio, and where lump sum additions are the primary deployment mode:

| Direct Plan Index Fund | Nifty 50 ETF | Difference | |

|---|---|---|---|

| Starting Corpus | ₹25,00,000 | ₹25,00,000 | — |

| Expense Ratio | 0.50% | 0.35% | 0.15% |

| Annual Cost | ₹12,500 | ₹8,750 | ₹3,750 saved |

| Growth Rate Assumed | 12% p.a. | 12% p.a. | — |

| Corpus After 15 Years | Lower by ₹1.5–2 lakh | Higher by ₹1.5–2 lakh | ~₹1.5–2 lakh |

Note: Calculation is illustrative. Actual difference varies based on ETF selected, broker transaction costs, and market returns.

Intraday pricing becomes useful. When deploying ₹5–10 lakh in a single transaction, the ability to buy at intraday prices using limit orders — rather than accepting end-of-day NAV — provides meaningful price control, particularly during high-volatility periods.

Portfolio transparency improves.

A core structured as Nifty 50 ETF + Nifty Next 50 ETF + Bharat Bond ETF is simpler to understand, monitor, and rebalance than a collection of four actively managed mutual funds with overlapping holdings.

The demat account is already active. Investors at Stage 4 with a ₹25 lakh+ corpus typically already maintain a demat relationship for direct stocks or PMS. Adding ETF purchases adds no new operational complexity.

The practical phase shift looks like this:

| Age Band | RSW Stage | Deployment Mode | Recommended Approach |

|---|---|---|---|

| 30–42 | Stages 2–3 | Monthly SIP | Direct plan index fund as core equity vehicle. ETF only as a supplement for lump sum additions if demat is already active — otherwise index fund alone is sufficient |

| 40–50 | Stage 4 | Mixed SIP + Lump Sum | ETF increasingly appropriate as core instrument for lump sum deployment. Direct plan index fund SIP continues in parallel for monthly surplus |

| 48+ | Stage 4 → Stage 5 | Predominantly Lump Sum | ETF-heavy core with Gold ETF and Bharat Bond ETF for asset class diversification. Actively managed funds retained only where a specific alpha thesis is being monitored. Progressive simplification begins |

Your Wealth Personality and the ETF Decision

The RSW Framework introduces Wealth Personality as a foundational assessment before any instrument recommendation is made.

It matters significantly in the ETF context — because the same ETF can be the right instrument for one investor and structurally wrong for another, not based on corpus size alone, but based on how they relate to their investments behaviourally.

The Passive Compounder — values simplicity, trusts systems over decisions. A Nifty 50 ETF bought and held across market cycles fits perfectly. The risk: temptation toward thematic or sectoral ETFs that demand active monitoring. The right architecture is a deliberately simple two or three ETF core — and nothing else.

The Active Engager — follows markets closely, comfortable with periodic rebalancing. Suits a Core and Tactical structure — broad ETF as anchor, sectoral or factor ETF as a sized, thesis-driven satellite. The risk: the tactical layer gradually expands, converting a disciplined portfolio into a collection of bets. Hard position limits are non-negotiable.

The Delegator — prefers guidance over self-directed management. A direct plan index fund within an advisor relationship is more appropriate than a self-managed ETF portfolio. Without structured check-ins, behavioural errors in an ETF portfolio compound quietly and go uncorrected.

Wealth Personality is not a fixed label. It shifts as your financial sophistication, life stage, and portfolio complexity evolve. The right ETF architecture evolves with it.

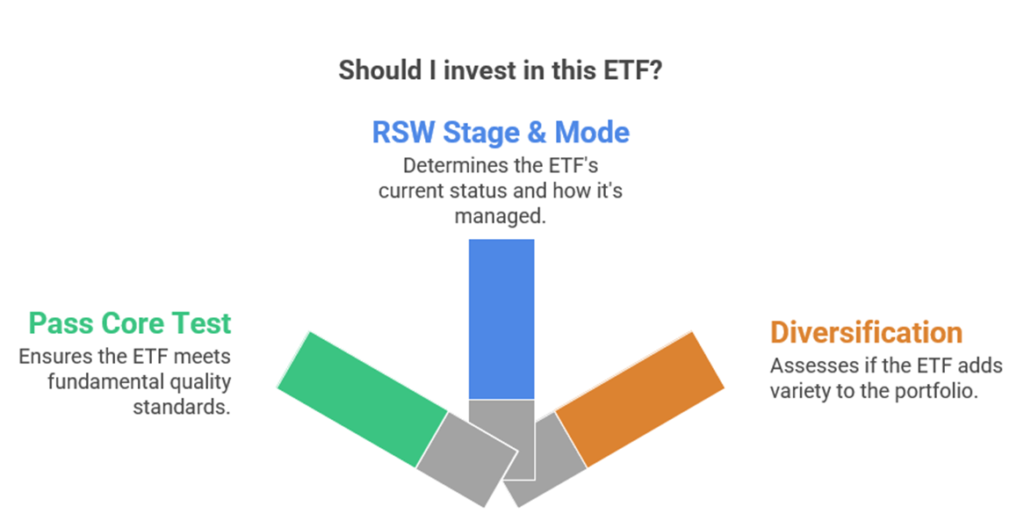

Your ETF Decision Map — A Three-Question Filter

Before adding any ETF to your portfolio, run it through these three questions.

If you hold a diversified equity mutual fund portfolio and are adding a Nifty Bank ETF because banking “looks attractive right now” — you are layering sector concentration onto a portfolio that was designed to avoid it. That is a tactical decision requiring its own justification, its own position sizing, and its own exit criteria.

Not an impulse.

The Behavioural Trap That Most ETF Articles Do Not Name

The greatest risk with ETFs is not tracking error, expense ratio, or SIP friction.

It is the illusion of sophistication that sectoral and thematic ETFs create.

An index fund is honest — you earn the market return, nothing more. An actively managed fund is accountable — the manager’s decisions can be evaluated.

A sector ETF sits in a false middle ground. It feels passive because it is exchange-listed and low cost. But it demands the same sector judgment a professional applies — when to enter, how long to hold, when to exit. The difference: the fund manager does this full time. You are doing it alongside a full-time career.

Most investors enter with a valid thesis. Few have a clear exit plan.

The RSW Framework’s principle applies directly: structure precedes performance. Size tactical ETFs strictly. Define the thesis before entering. Set exit conditions before the emotions arrive.

You now have the framework. The next step is applying it.

A structured review through the RSW Financial Independence Framework can map your current position, identify the gaps, and give you a clear sequence for what to do next.

No commitment. No products pushed. Just clarity.

An ETF bought without this structure is a position. An ETF bought within it is a plan.

Book your free one-hour wealth planning call →

Founder R S W Personal Finance Advisors.

B.E , PGDM [Marketing] ,

Chaterered Wealth Manager,

PMS Disributor, Mutual Fund Distributor.

Passionate about Personal Wealth Management. Practising 4+ Years.

Read more “About Me”